Finalist: The Post and Courier, by Tony Bartelme

Nominated Work

By Tony Bartelme

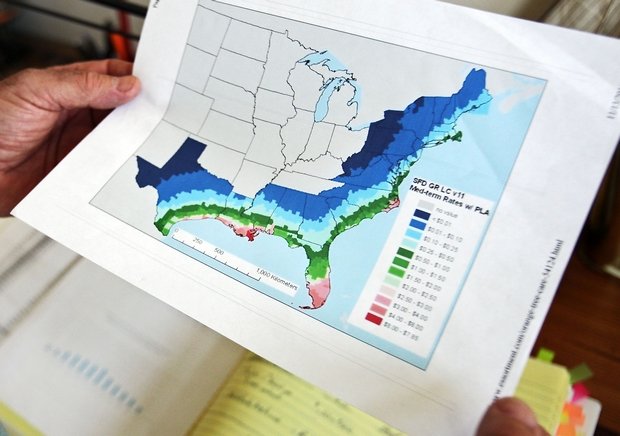

This is one of many documents that Daryl Ferguson has used in his research on insurance risk and rates.

Some things are certain: As the earth spins, air moves swiftly around the equator, creating the trade winds.

It's also certain that storms will form because the sun shines bright where these trades blow, turning sea water into sky-high clouds of steam that inevitably collapse, a process announced by torrents of rain and thunder.

And we know for sure from history and physics that a few of these air masses will spin counterclockwise, slowly at first, then faster and with enough momentum to flatten cities, alter destinies, and if hooked into some fantastic electric grid, pack enough energy to light every bulb on earth.

Beyond these certainties, hurricanes challenge us with their unknowns. They are so infinitely changeable that it may be mathematically impossible to predict their exact paths more than a few weeks in advance.

Because we can't predict the future, the beginning of hurricane season is a time of warnings and pleas to prepare. Like the humidity, anxiety settles in for the summer.

South Carolinians also try to tame this uncertainty by forking over $1.3 billion in homeowner's insurance premiums every year. How insurance companies set these rates is a story that touches all of us, but especially those who own homes in coastal counties.

It's a story that leads to globally recognized scientists, including some with data that show a home on the coast might not experience catastrophic hurricane winds for hundreds of years.

It features profit-seeking insurance companies that hiked rates, frustrated homeowners who scrambled to pay for these increases, and brilliant researchers who invented controversial computer models dubbed “black boxes.”

It shines a light on South Carolina's insurance regulators, who for the past decade watched rates soar but did almost nothing to find out how these secret black boxes truly affect homeowners' rates.

It could begin almost anywhere, but why not start at a cocktail party?

Three years ago, Daryl Ferguson and his wife were mingling with friends in Beaufort when a familiar topic came up: “Have you been watching TV?” a retiree from Connecticut asked Ferguson. “A hurricane is tracking right at Beaufort County.”

Another friend chimed in: “They don't hit us that often, but when they do it's awful. We almost got wiped out in 1893.” These fears got personal when two friends told Ferguson after church that they were moving back to Ohio. “I said, 'You guys love the Lowcountry, why are you leaving?' And my friend said that his wife just worries about the hurricanes all the time.”

Ferguson began to wonder: What is the true risk?

Ferguson, 73, isn't your ordinary retiree. He jabs the air when he makes a point and has an authoritative voice that seems to echo even in a carpeted room. For 10 years, he was president of Citizens Utilities, then the largest diversified utility company in the nation.

(Editor's note: Earlier versions of this story misidentified Ferguson's role with the utility. The Post and Courier regrets the error.)

Between 2000 until his retirement in 2005, he was chairman of Hungarian Telephone, sometimes matching wits with Russian mafia figures. “I like complex problems,” he said. So three years ago he began to learn about the complexities of hurricanes.

Ferguson's first call was to the National Hurricane Center, the National Oceanic and Atmospheric Administration's concrete fortress in Miami. He spoke to the head of the center's science unit and other meteorologists. He filled binders with charts and notes.

Over time, Ferguson learned how the jet stream undulates like a dropped firehose across the United States, but that it tends to twist south in the fall, sending tropical storms south into the Gulf of Mexico or north toward the Outer Banks, away from South Carolina.

He felt more reassured as he discovered that wind fields on the west side of hurricanes usually are smaller and weaker than on the east side. He learned about a quirk in South Carolina's geography.

South Carolina is triangular, like a poorly cut piece of pie, with the crust side facing the ocean. This triangle is positioned in such a way that the northern part of the coast juts about 150 miles farther into the ocean than the southern section.

Put another way, North Myrtle Beach is 150 miles closer to the Atlantic hurricane lanes than Hilton Head.

The concave shape of the coast makes the area from Charleston to Jacksonville less vulnerable to hurricanes, said Chris Landsea, science and operations officer at the hurricane center, one of the experts Ferguson contacted.

“South Carolina does indeed get struck by major hurricanes,” Landsea said, but the state's risk “is relatively lower” than Florida, coastal Louisiana and North Carolina's Outer Banks.

Ferguson heard similar statements from other forecasters. “I was stunned. They all kept saying the words 'relatively low risk.'”

Relatively low risk? In Ferguson's mind, that went against the conventional wisdom that South Carolina is a hurricane magnet. It also seemed at odds with history.

Since 1851, 30 hurricanes had spun within 50 miles of South Carolina, according to NOAA records. That was one about every five years, which seemed to be the definition of vulnerable.

But a closer look at the data was revealing: Of these 30 storms, 23 were minor hurricanes, such as 2004's Charley and Gaston, which caused minimal damage.

The remaining seven had winds greater than 110 mph and indeed wrought devastation where they had gone ashore. The Sea Islands Hurricane of 1893 killed as many as 2,000 people around Beaufort; Hugo in 1989 took 26 lives in South Carolina and caused $6 billion in damage.

But even these catastrophic hurricanes often left large swaths of South Carolina unscathed. Hugo, for instance, did little damage south of Seabrook Island, and more than half of the state saw winds of less than 60 mph.

So while it was correct to say seven major hurricanes had touched some area in South Carolina since 1851, about one every 23 years, that didn't really say much about the long-term vulnerability of a particular house in Beaufort or Charleston.

And in the end, Ferguson asked himself: Don't people want to know what's likely to affect them personally?

When scientists look at specific locations instead of areas as large as states, the odds of a home being hit by a hurricane change dramatically.

Kerry Emanuel is a professor of atmospheric sciences at the Massachusetts Institute of Technology and one of the world's leading authorities on hurricanes. At The Post and Courier's request, Emanuel's company, WindRisk Tech LLC, looked at 14 places along South Carolina's coast to see what kinds of winds these spots might experience over time.

Most scientists use historical data on wind speeds, barometric pressures and other variables to make their predictions, even though they acknowledge that this data has its shortcomings.

Some observations go back to the mid-1800s, but truly reliable measurements have been taken only in recent decades.

Statistical analyses typically need vast amounts of data to be accurate, but Emanuel and other modelers overcome this dearth with a neat bit of mathematical sleight of hand: Using principles of physics and other factors, they generate tens of thousands of virtual hurricanes on their computers. Doing this creates an archive equivalent to 5,000 years of storms, he said.

The computer simulations showed that a point in Charleston was likely to experience 74 mph winds, or a minimal Category 1 hurricane, about every 37 years over a 5,000-year period. The model showed that a catastrophic hurricane, one with 115 mph winds, would on average affect a spot in Charleston once every 370 years.

The situation on Hilton Head was even less threatening. A Hilton Head homeowner would be expected to experience a minimal Category 1 storm every 51 years, and a Category 3 storm about every 430 years, the WindRisk model showed.

Emanuel, Landsea and other experts cautioned that these calculations, known as “return periods,” don't predict the actual timing of a hurricane's next visit.

“Hurricanes don't care what happened last year,” Landsea said. “You can get hit twice in one year, or one year after the next. So the return period is more of an abstraction.” But the studies do give people some idea of their vulnerability to hurricanes.

To Ferguson, data like this was a bombshell.

It meant that while South Carolina as a whole was likely to experience minimal hurricane-force winds every few years, the risk of those winds affecting him personally were about once every half century.

It meant that the truly disastrous ones were rare and certainly not the impending train wrecks that weather channels and emergency planners sometimes suggest are on the way.

But if that was all true, he wondered, why were his insurance rates so high?

South Carolinians pay on average about one-third more for their homeowners' insurance than property owners in North Carolina and Georgia, according to a Post and Courier analysis of data from the National Association of Insurance Commissioners.

Last year, South Carolina insurers and the state's wind pool collected $1.3 billion in home insurance premiums, nearly three times what they charged in 1996. Statewide, average premiums have risen 71 percent during the past decade.

But this average understates the impact in coastal counties. The average premium for someone with $150,000 in insurance is about $2,000 in Charleston County and $1,840 in Beaufort County.

The farther inland you go, the less you pay. In Berkeley County, the average premium is about $1,200; in Dorchester County, it's $1,000, and upstate in Greenville County, it's only $720, according to S.C. Department of Insurance records.

Today, it's not unusual for some Lowcountry homeowners to pay more in insurance than property taxes. How did it get so bad?

The S.C. Insurance News Service, a nonprofit group funded by insurance companies, cites a mix of factors: dramatic growth in coastal South Carolina; rising property values; increased building costs; and new meteorological predictions that the world has entered a period of higher storm frequencies.

But it's also helpful to rewind to 1989, when Hugo rammed like a cannonball into South Carolina's midsection. John Richards was the state's insurance commissioner at the time. “We hadn't had much experience with catastrophes in the modern era until Hugo.”

The storm caused $6 billion in damages, which at that time made it the most expensive insurance disaster in the nation's history.

It also was a shining moment for the industry. Teams of agents swooped in. Amid the debris, they often wrote checks on the spot; billions of insurance dollars spurred a building boom. Richards said only two small companies were shut down because they were insolvent. Lawsuits were rare. “The insurance companies did a wonderful job after Hugo,” he said.

But it marked the end of an era — in meteorological terms and in insurance company boardrooms.

Scientists had long wondered why there had been a lull in Atlantic hurricanes from the 1940s until the early 1990s. Some researchers theorized that it was a natural climate cycle called Atlantic Multidecadal Oscillation.

Then Kerry Emanuel and Michael E. Mann, a prominent Penn State climatologist, noticed something else: Hurricane frequency seemed to correspond to pollution levels in the tropics.

They found that pollutants rose dramatically from the 1940s through the 1970s as the world's industrial production grew. These pollutants reflected sunlight, reducing the amount of energy hitting ocean waters in the tropics, the heat source that gives birth to the storms.

“We had suppressed them,” Emanuel said of the hurricanes.

But those pollutants began to dissipate with new clean-air laws in the 1970s and 1980s. More sunlight reached the tropics by the early 1990s. Emanuel and Mann theorized that the warming oceans in the tropics would fuel a frenzy of new storms, a theory supported by subsequent studies.

Meanwhile, insurance companies thought Hugo was an aberration, said Richards, the former South Carolina insurance commissioner. “They thought, Thank goodness, this is just a storm we'll never see again for a decade or two.”

Even after Hugo, insurance experts assumed that storms in heavily populated Florida would cause damages in the low billions of dollars, losses they figured they could swallow.

Then Andrew hit South Florida in 1992. It was a compact hurricane, more like a giant tornado; hurricane-force winds formed a bullet of wind 40 miles wide that entered south of Miami, churned through the Everglades and exited into the Gulf just four hours later.

Inside this maelstrom, 140 mph winds hammered the city of Homestead and other communities. Richards rushed south to help his colleagues.

“The night I arrived, I was in Tallahassee at the house of the Florida insurance commissioner. I said, 'One thing you have to be aware of is that your (insurance) industry is taking quite a hit. And you better send teams of examiners to those companies as soon as possible.' He laughed and said, 'John, I'm not worried.'”

Richards was right, of course. Andrew caused about $16 billion in insured damages that triggered more than 600,000 claims. Eleven insurance companies went belly up, and the finances of dozens of others were shaken.

Tens of thousands of policyholders were left stranded. While those in Andrew's relatively narrow path began rebuilding, Allstate announced plans to cancel 300,000 of its 1.1 million policies in Florida and raise rates 32 percent, a plan it scaled back after furious protests from homeowners.

Richards said the relationship between insurance companies and homeowners began to sour.

“After Hugo, lawsuits against insurance companies were in the dozens, but after Andrew, they were in the thousands. It shows there was a different climate after Andrew.”

Hurricane Andrew was particularly helpful, though, to a woman in Boston named Karen Clark, head of a little-known company called Applied Insurance Research.

While other insurers had predicted potential insurance losses in the low billions of dollars, Clark had warned that a major South Florida storm could generate a $30 billion insurance industry hit.

Her calculations were based on a novel way of looking at risk.

In the past, insurance companies tallied potential losses in a particular area and stopped writing new policies when they felt their exposure was too high. But Clark questioned how you could truly understand risk without knowing your odds of being harmed.

So she plugged historical data on hurricane strikes into computer programs along with data about homes and buildings — potential losses for anyone who insured these structures.

Then she ran computer simulations of what might happen in various scenarios.

Her success in predicting losses before Andrew launched the new industry of “catastrophe modeling.” Other companies soon created their own models, which became known in the industry as “black boxes” because their algorithms and inputs were kept secret for competitive reasons.

These mysterious black boxes would increasingly determine what homeowners from the Gulf Coast to New England shelled out in premiums.

During his career as a corporate executive, Daryl Ferguson had moved to different cities across the country, but when he finally retired on a bluff overlooking the Whale Branch River near Beaufort, he thought his property insurance seemed unusually high.

Now, with his new understanding of hurricane risks in South Carolina, he was even more convinced that his rates were out of whack.

“My insurance company, USAA, is terrific, so I did a test.” He asked company officials how much it would cost to insure a newly built $400,000 home in Gulfport, Miss., versus one in Beaufort County.

Gulfport had been hit hard by Katrina and Rita and is considered particularly vulnerable to hurricanes. “I couldn't believe what they told me.” His hypothetical Gulfport bill would be one-third the price of his Beaufort premium. “I turned to my wife and said, 'This is like Sherlock Holmes; one question leads to another.'?”

Ferguson had stumbled onto something. The average premium for $400,000 homes in South Carolina was the seventh highest in the nation, roughly the same as tornado-prone Oklahoma, according to the National Association of Insurance Commissioners.

“I was shocked,” Ferguson said. “My first instinct was to go to the Department of Insurance and ask them why they're approving these rates, but I decided to do some homework first.”

He began looking for Martin Simons.

Few people outside the insurance industry knew more about the black boxes than Simons, a bookish man with a scraggly salt-and-pepper beard who, unknown to homeowners, had long had a major impact on what they paid in insurance.

Between 1985 and 1997, Simons had been deputy director and chief actuary for the state Department of Insurance. In that capacity he had forced some insurers to reduce rates when their profits were too high and urged others to raise rates when his analyses showed they were too low. He left the agency when he felt state leaders had become too anti-regulation, and he had gone on to build a national reputation in the arcane world of actuarial analyses.

When Florida regulators established the nation's first independent panel to review how computer models affect rates, they hired Simons. He later did work for Maryland and California, and conveniently lived in Columbia.

Ferguson met Simons for lunch at the Chili's restaurant next to Simons' granddaughter's auto repair shop in Summerville.

“The first words he said to me were, 'Daryl, I know what you want.'” Ferguson was puzzled. “Then he said, 'You want to know why the Department of Insurance doesn't regulate its homeowner industry?' It was exactly what I wanted to know.”

Simons had long lamented the lack of transparency about the catastrophe models. In 2003, State Farm requested a 29 percent increase in its rates. This hike would ripple across the state because State Farm controls about 25 percent of the homeowner's insurance market.

State Farm justified the increase in part because of results from the black boxes.

At the time, the state Department of Consumer Affairs was charged with reviewing rate increases, and the agency hired Simons to scrutinize State Farm's proposal. In sworn testimony before the hearing, Simons said the request was “seriously flawed,” largely in part because state regulators knew nothing about how catastrophe models work.

The stakes were huge, he testified: Unscrupulous insurers theoretically could choose a model to set rates as high as possible. Or they could use a model's calculations to justify reduced rates to undercut their competitors, putting the company at risk if a storm struck.

“Eventually all property insurance premiums for hurricane coverage in South Carolina will be determined using the outputs of stochastic computer hurricane simulation models,” he testified, adding that the insurance industry also uses these black boxes to assess terrorism risks and in health, auto and life insurance calculations.

How the state deals with these models “will impact every citizen in this state.”

Minutes before the rate case was set to begin, State Farm settled for a 19 percent increase and an agreement that it wouldn't oppose an independent panel to examine catastrophe models.

That review didn't happen.The Department of Insurance, with money from the S.C. Sea Grant Consortium, asked three experts to look at the models. One was Peter Sparks, a noted civil engineering professor at Clemson University who had done extensive studies about wind speeds and damage.

Sparks has found that the National Hurricane Center tends to overstate wind speeds inland, and that “an unwise modeler using National Hurricane Center reports could easily get a distorted picture of the wind climate and recommend rates far higher than justified.”

He said that when he and the other panel members asked the modeling companies for a look at the assumptions built into their black boxes, “They said that the information was proprietary and would not disclose their methods. We said we could not judge the soundness of them, and the Department of Insurance eventually abandoned the whole exercise.”

Meanwhile, the General Assembly eviscerated the budget of the S.C. Department of Consumer Affairs, the government's main insurance watchdog.

The department lost half of its employees over the past five years; today, it has about 30 staff members to cover thousands of consumer complaints and insurance issues, one-third the roster of the University of South Carolina football team.

In 2007, amid threats that insurance companies would abandon coastal areas, lawmakers also stripped the agency of its ability to challenge rate increases below 7 percent. That meant, in effect, that an insurance company could raise rates almost at will as long as its average increase was below 7 percent. “We've had a lot of 6.9 percent rate increases since then,” said Elliott Elam, the state's consumer advocate.

To Simons, insurance rates involve finding a delicate balance between a company's capacity to make money and a homeowner's ability to pay. And in the absence of a serious review of these black boxes, he feared that homeowners on the coast are getting crushed.

Ferguson said alarm bells went off when he heard Simons talk about this imbalance.

As a former CEO of large and heavily regulated utilities, “I had first-hand knowledge about what happens when a state doesn't regulate,” he said. It meant millions of dollars could be added to the company's bottom line, and millions subtracted from customers' pockets.

Experts acknowledge that no computer model can predict the future, but a new iteration of computer models has taken a step in that direction. These new models use data on warming oceans and other variables to forecast potential hurricane losses in a five-year period.

In the mid-2000s, these models predicted a major increase in hurricane losses, and as a result, insurance companies sought rate increases and pulled out of coastal areas in South Carolina and elsewhere, triggering what was widely described as an “insurance crisis.”

So far, the predictions of these new models haven't panned out, said Karen Clark, the architect of the original black box. In a study, she found that they overestimated losses by as much as $53 billion.

Clark told The Post and Courier that catastrophe models are useful but crude tools, and that it makes little sense to predict hurricane losses in the near term when meteorologists struggle to predict how many storms might form in the coming hurricane season.

“Trying to project hurricane experience over a short-term horizon is inherently flawed,” she said.

Then again, the use of catastrophe models has “added a degree of stability to the insurance market that wasn't there before them,” said Michael Young, a senior director with Risk Management Solutions, the largest of the modeling companies. The industry's performance is proof, he and other insurance experts said.

While many companies went belly-up after Hurricane Andrew, only one went under after the devastating hurricanes in 2004 and 2005. Last year, despite horrific losses worldwide and in the United States, the U.S. property and casualty industry made $22 billion in profits.

In Beaufort, Ferguson pages through notebooks he has compiled during his investigation. From his upstairs window, the marsh in the Whale Branch River shimmers in the heat. He estimates that he has spent 2,000 hours on this project, time that gave him new appreciation of the mysteries of the Lowcountry and fewer reasons to fear that a hurricane will blow it all away.

“We have plenty of time to get out of the way if a storm does come our way, so the risk isn't about people anymore; it's about property.” As he grew less fearful about hurricane season, he thought about the opportunities this new perspective presents: How a regional campaign to promote Lowcountry tourism in the fall could generate thousands of new jobs, how an in-depth look at insurance rates by state regulators could stimulate the economy like a tax cut.

With homeowners shelling out $1.3 billion in premiums, even a small percentage reduction could mean tens of millions of dollars.

But as stores put up hurricane displays, and emergency officials issue fresh warnings to get ready for the hurricane season, the questions in Ferguson's mind continue to spin, especially when he goes to a picnic on Memorial Day and hears what happened to his friends.

They live in Bull Point, a subdivision well inland from Beaufort, and they had just received a letter from their insurance company canceling their insurance effective Aug. 29. The reason: catastrophic wind exposure.

“Why?” he asked out loud after seeing the letter. The company hadn't explained its reasoning, or given his friends a chance to discuss the issue. “Overall, this looks like a monopoly gone wild,” he said, “and the only one that loses is the customer.”

***

What is a black box?

When it comes to insurance, you can't drop a “black box” or use it to record pilots before they crash a plane. The term is used in insurance circles to describe computer programs that analyze historical data and information about houses and buildings.Karen Clark, founder of AIR Worldwide, began using these programs in the late 1980s and early 1990s to analyze potential losses in the event of a hurricane. Other companies, such as Risk Management Solutions, have models of their own and have created programs to analyze potential losses in earthquakes and other disasters.Companies zealously guard their programs for competitive reasons, hence the term black box. Florida, however, has established a panel of independent experts to scrutinize these models because of their importance in rate-setting.

By Tony Bartelme

Mark Romano, a former Allstate executive turned whistleblower, stands outside the fence circling Allstate's massive guarded headquarters in Northbrook, Ill., a suburb of Chicago. Romano was in charge of a computer program called "Colossus" that calculates money people are paid in claims. Romano "tuned" the program to increase profits, which he says was unfair to customers. Photo by Tony Bartelme

Mark Romano gripped the steering wheel and tried to keep his car from swerving into another commuter on the busy Illinois tollway.

“God, please don’t let me hurt someone,” he prayed.

Dizzy again. These bouts of vertigo were barely noticeable at first, but something else was going on now. At night, he would lie in his bed, stare at the ceiling and watch everything twirl. In the morning, the spells came in waves during his commute to Allstate’s national headquarters in suburban Chicago.

Stress?

It was December 2007, and Romano was a senior manager at Allstate and its top expert in Colossus, a program that calculates how much a person might be paid for an injury claim. He was in charge of two projects to “tune” and “recalibrate” Colossus, work he knew could affect payments to thousands of people.

Colossus was part of a quiet revolution in the insurance industry.

Before the early 1990s, insurance was a decidedly human endeavor, especially when it came to setting rates and paying claims. To set premiums, insurers relied on computations from their actuaries — mathematical wizards armed with statistics and tables that assess various risks. When it came to paying claims, insurers often sent adjusters into the field, where they met face-to-face with people injured in car wrecks.

Today, insurers have an array of computer programs that guide the flow of trillions of dollars to and from customers around the world. These programs include sophisticated “catastrophe models” that use weather data and other factors to predict an insurance company’s losses in a disaster. “Scoring models” use credit histories and secret algorithms to estimate which customers are more likely to file claims. Colossus and similar programs help companies manage claims. Like a TurboTax program for medical injuries, adjusters plug in information about a person’s loss — from a damaged spine to a fractured finger. Colossus then cranks out a range of payments to cover the costs. Insurance industry critics and even many insiders call these programs “black boxes” because their formulas, data sets and operational policies are cloaked in secrecy.

Few people at Allstate knew more about Colossus than Romano. On organizational charts, he was Allstate’s Colossus “subject matter expert.” And in late 2007, at age 49, he was at the peak of his career, working in one of the nation’s largest insurance companies — and wondering whether he should leave it all behind.

Romano has thick black hair and wears thin glasses. His brown eyes widen when he wants to make a point. He had gone into the business to help people, but he knew that his work on Colossus would do the opposite.

During his hourlong commute to Allstate’s sprawling campus in Northbrook, his mind drifted to his daughter at the College of Charleston, to his son in private school, his wife’s multiple sclerosis, medical bills, his mortgage, the decades he put into his career. The dizzy spells grew worse. Doctors prescribed motion sickness medicine, relaxants and physical therapy. Then the headaches came — migraines as long and powerful as a Midwestern freight train, box cars of pain, one after another after another. Something had to give.

Among computer programmers, the name Colossus has a rich history. In World War II, British code-breakers called their hulking new programmable machine Colossus and used it to decipher German teleprinter messages. In 1970, filmmakers released “Colossus: The Forbin Project,” a science fiction movie about an army supercomputer that tries to take over the world. (At one point, the computer tells its human creator, “You will come to regard me not only with respect and awe but with love.”)

The insurance industry’s version of Colossus was born in Australia. In the 1980s, a government-chartered insurer ran into financial trouble because of claim costs, which were growing at an annual rate of 14 percent. The insurer set its sights on its adjusters.

It’s the adjuster’s job to evaluate people’s losses and come up with ways to settle their claims. This often meant assessing what people did in their careers and how an injury might affect their future income and overall enjoyment of life. Longtime adjusters talk about the challenge of sizing up people when they’re suffering, and the knowledge adjusters need, from medicine to car repairs, to calculate a fair settlement.

The inherent complexity in putting numbers on injuries also meant that adjusters often came up with different amounts for similar types of claims. In Australia, payments varied by more than 80 percent. So to reduce these disparities and lower overall costs, the Australian insurer worked with a software company on a novel idea: embed the experience and knowledge of their best adjusters in a computer program.

The programmers studied how top adjusters made decisions and then created software to mimic their work. This program became known as Colossus and required answers to as many as 700 questions, ranging from the severity of injuries to how people experienced the loss of enjoyment in life. Injuries were broken down into 600 different codes. The program analyzed legal settlements and jury verdicts, combined this information with data entered by the adjusters, and generated what were supposed to be fair settlements.

A few people questioned whether computer programs were up to this complex task. An Australian law professor wrote that the development of Colossus was “just one instance of an important challenge of the information age: how to ensure that computer-based decision making is fair and non-discriminatory.” But Colossus was a huge success. Within a few years, payments for similar claims were more consistent and the costs of those claims had stopped rising.

In the United States, the insurance industry was experiencing its own period of self-analysis. It began in 1989, when Hurricane Hugo flattened parts of South Carolina. The storm caused $4.2 billion in damage to insured property — at the time the most expensive loss in history. The second wake-up call came in 1992 when Hurricane Andrew generated $15.5 billion in claim payments, $10 billion more than actuaries had predicted. Andrew bankrupted 11 insurance companies and prompted dozens of others to flee the Florida market altogether.

Amid this sticker shock, industry leaders asked why they had so badly underestimated their potential losses. They found answers in newly created “catastrophe models,” computer programs that predicted potential damages in a hurricane or other disaster. These models warned that future hurricanes would be even more costly, and with these new predictions in hand, insurers soon justified massive rate increases in home insurance premiums, especially in South Carolina and other coastal states.

While insurance premiums are the insurance industry’s main source of income, payments for claims are its biggest costs, the equivalent of rubber for a tire manufacturer. Claims also are at the heart of why people buy insurance. Insurance is based on the idea of sharing risk, a grand communal exercise that involves collecting $4.6 trillion every year from people across the world and then shifting some of this to a smaller pool who suffered losses. Insurance keeps communities destroyed by disasters on life support until their economies recover; it helps keep people out of bankruptcy after car wrecks and house fires. And it was largely for these noble purposes that Mark Romano decided to make insurance his life’s work.

Romano grew up in Tampa, Fla., and by his account had a relatively uneventful childhood. He loved catching and dissecting animals for biology classes and thought someday he might go into medicine. He played trombone in the high school band. His mother was a school librarian. His father was regional director for the Florida Department of Agriculture and Consumer Services, and Romano remembers his dad coming home angry about how consumers had been bilked in one way or another. After high school, Romano enrolled in Florida State University, where he gravitated toward the school of insurance and risk management. “I was interested in the basic concept of risk, that you could transfer it from one person to an entity or spread it among many people,” he said. “And you were helping people, and I grew up with two parents who in one way or another helped people.”

Romano’s first job was as an adjuster with American States Insurance, and his first day at work came after a drenching Florida rainstorm. His boss told him to grab a map and clipboard and take measurements of damaged homes. “It was overwhelming, but it was cool,” he said. “I absolutely loved being on the road. Everything was face to face, and it would be very common to meet people in their homes, sit in their kitchen and talk about their injuries.”

Romano handled auto insurance claims and worker’s compensation cases, learned about medicine, the law and how to establish rapport with people in distress. “You did it all, and it was an incredible education in how the world works.” Not all of this education was positive. A year into his career, he took over a new territory, and when he introduced himself to auto repair shop owners, “One guy said, ‘Hey, do you want the same deal as the other guy?’ ” Romano wasn’t sure what to do. “I went to my father and said, ‘These people are offering me things.’ And he said, ‘Don’t you dare ever do anything like that.’ That’s how naive I was at that point.”

But the vast majority of those he met were “really good, decent people trying to put their lives together.” He remembered a case in which he helped a family set up a scholarship to honor their child, who had died in a car wreck. By then, Romano had moved to another company, Hanover Insurance, which had a charismatic chief executive officer named Bill O’Brien. “For him, it was all about empowering employees at the lowest level possible. And we were never told to watch or shave anything off a claim payment.” If a customer’s claim was too low, it was the adjuster’s duty to pay them more. “You really felt good about what you were doing.”

Then, after Hurricane Andrew in 1992, Hanover Insurance started closing offices in Florida. It also was a pivot point for Romano. He was mid-way into his career and eager to advance. The place to do this was Chicago, a mecca of property and casualty insurance. He would take a circuitous route to get there, though. He left Hanover and took a job at CNA insurance division in upstate New York, where he learned about a program called Colossus.

By then, the Australian creators of Colossus had sold the program to Computer Sciences Corp., now named CSC, which licensed it to Allstate and many other insurance companies.

CSC’s marketing materials have long touted Colossus as a way to help insurers “establish consistent recommended settlement ranges,” Edward Charlton, a CSC vice president, said in a statement to The Post and Courier. “Without a clearly defined process or framework in place provided by a software tool such as Colossus, claim adjusters may skip important steps or forget to ask pertinent questions of consumers,” he said.

In Romano’s mind, it made good business sense for companies to automate claim payments, though he feared something could be lost without a more personal touch. And based on his years working as an adjuster, the payouts Colossus spit out for CNA seemed fair. He excelled in his job and eventually was transferred to CNA’s bright red headquarters on Chicago’s Wabash Avenue. As he walked into the building, he looked at the skyline. All around were skyscrapers adorned with the names Prudential, Blue Cross, Kemper and Hancock, huddled like giants overlooking Lake Michigan’s southern arc.

Allstate was created a year after the stock market crash of 1929, when Robert Wood, president of Sears Roebuck & Co., boarded a commuter train to downtown Chicago. On his ride in, a friend suggested he start an auto insurance company and sell insurance by mail. Wood eventually formed a company called Allstate Insurance Co., naming it after a tire sold in the Sears catalog. In 1950, the daughter of a sales manager came down with hepatitis. When the sales manager returned home, his wife reported, “The hospital said not to worry. We’re in good hands with the doctor.”

Thus, the iconic slogan was born: “You’re in Good Hands with Allstate,” along with the logo of a pair of hands cradling a car. (The car was later removed.) By 2000, the “Good Hands” phrase was the most recognized advertising slogan in America, according to a Northwestern University study. Allstate became one of the industry’s largest insurers, and grew even more in 1999 with the $1.2 billion acquisition of CNA’s personal insurance division.

Romano heard rumors about the deal months before it was made public. A senior vice president approached him and said, “Mark, I hear you know something about Colossus.” The executive told him Allstate was looking for someone to implement their version of Colossus on CNA’s customers.

Allstate renamed the CNA division Encompass, and Romano soon met with Allstate executives who, he said, “began indoctrinating me in their Colossus philosophy.”

Romano discovered that if he used Colossus the way Allstate did, he could save its new Encompass division millions of dollars by “turning the knobs” of the software — paying people less in claims than they would have otherwise gotten.

In South Carolina, for instance, CNA had divided the state into two territories — the “Liberal” area around Charleston and the “Conservative” region elsewhere. Allstate renamed the territories “Charleston” and “Palmetto.” By using Allstate’s Colossus tuning methods instead of CNA’s, Romano could reduce payments in the Palmetto region by 18 percent. Savings were even greater in the Charleston area — a 57 percent reduction. That meant the Allstate version of Colossus would turn a $10,000 claim in Charleston into a $4,300 payment.

“It became my responsibility and goal to save $33 million over three years for Encompass, which I did.” (In a statement to The Post and Courier, Allstate did not dispute Romano’s account but said government regulators have examined its tuning methods and found no violations of state statutes.)

Romano was so successful that Allstate transferred him from the Encompass office downtown to Allstate’s headquarters. Now, instead of downtown Chicago, his commute took him to suburban Northbrook and a 250-acre office park surrounded by fields, security fences and guard gates. “They sent me to the mothership.”

About the same time in 2000, Rob Dietz was working as an adjuster for Farmers Insurance Group in the Seattle area. Like Romano, he felt a sense of purpose helping people put their lives back together. A former logger and rock blaster, Dietz became an adjuster, he recalled, because “it was easier to lift a pen than a chain saw, and because it served the public.” Unlike Romano, he was almost immediately appalled by Colossus.

Farmers was just beginning to implement Colossus. As part of that effort, the company asked Dietz and other experienced adjusters to examine a sample of claims and come up with fair offers to pay people for their losses. These offers would be fed into Colossus to create a benchmark of payouts tailored to that area of the Northwest. But after the group finished, a facilitator said the ranges would then be reduced by 20 percent to create even lower benchmarks.

Dietz was stunned. To him, it meant that the program was being rigged to make payments 20 percent lower than they should have been. “That’s not how I learned the tenets of good faith and fair dealing.”

Worse, after this session, he said he and his colleagues were under constant pressure to stick with Colossus-generated payments even when the adjusters thought people deserved more. He felt Colossus was turning his profession into keyboard slaves, and for a “person with logger’s fingers,” this didn’t bode well for his career prospects. He was also taken aback by the secrecy around Colossus. “I still have the old memo that says we were not to disclose the fact that we were using Colossus.”

Dietz eventually quit Farmers to work with trial lawyers, and in 2002, a Washington State attorneys group asked him and another adjuster to give a talk about Colossus. “That’s when Farmers sued me.”

Farmers asked a judge to stop the seminar, arguing that Dietz and the other adjuster would reveal confidential information. The judge declined, and Farmers eventually dropped the suit. Lawyers from all over the nation flew in for the talk. Aaron DeShaw, an attorney investigating Colossus, remembers how he and the other attorneys gave Dietz and the other adjuster a standing ovation before they opened their mouths. “The atmosphere was electric.”

This was the beginning of what would become a decade-long legal assault on Colossus and other claim-handling programs, one that would somehow bypass Romano, despite his extensive work at Allstate with the program.

One of the most aggressive pushes came from David Berardinelli, a trial lawyer in Santa Fe, N.M., known for his love of vintage Porsches and a book he wrote about his battle with Allstate, “From Good Hands to Boxing Gloves.”

He learned about Colossus while representing a husband and wife hit by an uninsured drunk driver. Allstate refused to pay their medical bills, and curious about Allstate’s hardball legal tactics, Berardinelli sought internal presentation slides and notes about how the company handled claims. In one legal fight after another, Allstate refused to give them up, saying in a court document, it was engaging in “respectful civil disobedience.” At one point, Florida insurance regulators joined the fray, threatening to prevent Allstate from writing new policies unless the company handed them over.

Allstate eventually capitulated, and the materials provided a window into a company in flux. The most incendiary documents stretched back to the early 1990s. At the time, insurers were railing about what they considered a wave of frivolous lawsuits from lawyers who used aggressive advertising campaigns to lure clients. In 1992, Allstate hired McKinsey & Company, a consultant for the nation’s leading insurance conglomerates. One goal, according to a slide, was to “radically alter our whole approach to the business of claims.”

One of the McKinsey presentation slides described how the company could become more efficient if it targeted people who didn’t have lawyers. In its “Good Hands” approach, Allstate would pay those unrepresented people within 180 days, which McKinsey said would take care of 90 percent of the claims. The 10 percent who hired lawyers or didn’t accept claim offers would get the “Boxing Gloves” treatment. In these cases, Allstate would expect to tie up payments for three to five years.

Over time, Allstate employees testified that they were trained to build rapport with customers and discourage them from hiring lawyers. Berardinelli and a growing cadre of lawyers alleged that the “good hands” strategy actually involved delaying and denying claims for several months and then making lowball offers as people felt more financial pressure. They argued that Colossus and other claim-handling programs were important parts of this profit-making plan, with some testimony showing that Allstate could reduce bodily injury payouts by $264 million a year if it used Colossus. “This immediate impact would, of course, come at the immediate expense of Allstate’s policyholders,” Berardinelli wrote in his book.

In a 2008 press statement, Allstate said the materials were part of “a complex body of work that as a whole demonstrates a careful, fact-based analysis to better enable the company to more promptly investigate and more consistently and effectively evaluate claims.” Allstate told The Post and Courier that the software “provides merely a recommendation, and is only one factor in the adjuster’s overall evaluation of the claim.” Charlton, the executive with Colossus’ maker, CSC, said that his company leaves the tuning process to insurers.

Meanwhile, other industry officials have long discounted the importance of the McKinsey documents. Robert P. Hartwig, president of the Insurance Information Institute, said the notion that the documents “forever directed the entire homeowner and auto insurance process” was “bizarre.”

Rather, he said, such programs reflect an understandable use of technology. “There are millions of claims every year and a lot of commonality between them,” he said, adding that said Colossus and Xactimate, a Colossus-like program that handles home insurance claims, “harness the computer to process large amounts of data quickly and inexpensively, and that allows insurers to provide coverage that’s very affordable.” Insurers wage a “technological arms race against each other on a daily basis,” he said, and companies with the best technology have an edge. “This is a competitive industry, and it’s not in the insurer’s interest to treat a customer poorly.”

But Berardinelli and others alleged in class-action lawsuits that insurers were doing exactly that — failing to pay customers what they were due. More documents and testimony emerged, including manuals that described how tuning Colossus was “both an art and a science” that was done “based on the desired projected savings.” One slide from CSC said, “What does Colossus Really do” and begins with a list: “Lowers indemnity payouts ... lowers loss ratios ... improves surplus/profitability.” Other documents urged employees to avoid using the word “savings” to describe the benefits of Colossus and “use a more vague term such as ‘consistency.’ ”

One of the most prominent lawsuits involved a woman from Arkansas named Georgia Hensley. Hensley was driving on a road near Texarkana on New Year’s Eve 2000, when she was struck by an underinsured driver. She broke facial bones and injured her spine. She filed a claim with her insurer, Encompass, which offered $1,000. Hensley’s lawsuit alleged Colossus and other claim-handling programs were cost-containment tools that enhance insurance company profits at the expense of customers.

Hensley’s claim had been handled by one of Romano’s underlings, and Romano was one of the first at Allstate to learn about the lawsuit.

It landed in his email inbox on Feb. 17, 2005. Romano read the lawsuit, a class-action case that named hundreds of insurance companies that used Colossus and other claims-handling programs. He sent it upstairs to the attorneys. By then, he was beginning to feel the weight of his work.

His responsibilities had grown. His tuning directly affected how thousands of claims employees across the country did their jobs, and through them, how much tens of thousands of policyholders were paid for their losses. He was part of a small group of insurance professionals nationwide that met regularly to discuss Colossus-related issues.

These meetings often happened in warm places, including Myrtle Beach. Romano was glad to go to these particular meetings because it meant he could visit his daughter, a biology major at the College of Charleston. They grabbed sandwiches at Groucho’s on King Street and took walks to the Market, where he stocked up on Lillie’s of Charleston Low Country Loco hot sauce, grits and other Southern specialties tough to find in Chicago.

He didn’t talk about insurance, though. The issues he was wrestling with were complex, and he was more interested in how his daughter was doing. He also kept much of his worries from his wife. In 2003, she was diagnosed with multiple sclerosis, and he wanted her life as stress-free as possible. “I didn’t share my feelings about Colossus with anyone, but if I had talked about it, I would have said, ‘I’m doing some stuff that I’m not too thrilled to be doing.’ ”

In his mind, Colossus was as malleable as clay. You could mold its programs to reduce claims values across-the-board, which he described as “turning the knobs.” You could decline to enter data on high jury verdicts or unusually high injury settlements, which tricked the program into thinking an injury’s typical value was lower than it really was. You could train adjusters to code injuries in a way that didn’t account for their true severity, which also reduced payments.

In late 2007 and early 2008, even as the Hensley and similar lawsuits began to produce out-of-court settlements worth tens of millions of dollars, Romano worked on new ways to “recalibrate” and tune Colossus, projects that he said would generally “lower settlement values” and increase profits.

His migraines grew more severe. Doctors prescribed tranquilizers, ordered physical therapy sessions. Nothing helped. He couldn’t sleep. The dizzy spells became more jarring until the doctors told him to turn over his car keys. He temporarily left work and went on disability. Through this haze, he began to see other things more clearly: People were being hurt by Colossus, and it was tearing him apart. He couldn’t turn the knobs anymore.

On his last day at Allstate, he was told to hand in his laptop and badge. On the long drive home, he had no bouts of vertigo, only relief bordering on exhilaration. “It was the first step in regaining my self-respect.” He had a new quest: to help consumers better understand how the insurance industry can fail to live up to the promise of paying people in their times of need. He thought he would be part of a larger chorus, especially now that state regulators had turned their attention to Colossus.

In 2009, led by New York and Illinois, state insurance regulators began the first multi-state examination of how an insurance company uses a software tool to handle claims. Working with the National Association of Insurance Commissioners, the regulators hired a private company to sift through a million pages of claims data and other Colossus-related materials. Investigators later said they spent 8,500 hours reviewing the materials and interviewing more than 40 current and former Allstate employees.

The regulators announced their findings a year later: Overall, they found no “institutional issues involving underpayment of claims” but that Allstate failed to tune the software in a consistent way across the nation. “Colossus was a black box. We looked into the black box and saw some problems,” Steve Nachman, New York’s deputy superintendent for fraud and consumer services, told reporters at the time. “It’s all about how you utilize it.”

Among other things, the regulators ordered Allstate to tell consumers when they had used Colossus to calculate a claim payment. Allstate also was fined $10 million. More than 40 states signed on to the deal, including South Carolina, which received $235,166. (The money went to the state’s general fund.) In a news release, Allstate said the findings showed their use of Colossus “provides significant benefits to the public in increased objectivity and efficiency.”

In a statement to The Post and Courier, Allstate said the investigation in fact justified “the continued use of the tuning criteria which have now been used by Allstate for more than 15 years.” Colossus critics weren’t impressed with the fine or the findings. “Ten million dollars is no big deal,” said DeShaw, the trial lawyer in Washington. “They make that in no time.” (In 2011, Allstate had $32 billion in revenue and a profit of $788 million.)

“A part of this story is the failure of state insurance regulators to police insurance companies’ conduct,” added Jay Feinman, a law professor at Rutgers University and author of “Delay, Deny, Defend,” a book that says insurers try to avoid paying claims.

Robert Hunter, a director with the Consumer Federation of America, was blunter: “It was weak.” If the investigation was so thorough, he asked aloud, why had the regulators failed to talk with Allstate’s official Colossus expert, Mark Romano?

Romano asks himself the same question. The investigation was hardly a secret in Allstate’s hallways, he recalled. He said he even knew where the examiners worked — two miles away near an executive airport. At one point, he contacted an examiner, who told him it was too late to use his information; they had all but wrapped up their work. Romano eventually called Hunter at the Consumer Federation of America.

Hunter remembers the call. “One of the first things he said was that he wanted to help consumers, which is something I liked.” Hunter had already assembled a large body of information about Colossus but was happy to learn about Romano. “Suddenly we had a guy from inside who knew how it worked.”

Romano joined the group and co-wrote a paper last summer with Hunter: “Low Ball: An Insider’s Look at How Some Insurers Can Manipulate Computerized Systems to Broadly Underpay Injury Claims.” It generated numerous stories in insurance trade journals and websites, along with scattered newspaper reports, but Romano acknowledged that “Low Ball” was designed to raise interest among regulators, not the general public, and he’s not sure it made much headway.

These black boxes have a significant impact on what people in South Carolina receive for their claims, but state insurance regulators have no plans to study Colossus or other claim handling programs. They say they leave such analyses to states where insurance companies are based. Overall, said Robert Hartwig of the Insurance Information Institute, “these issues are dead and buried, and regulators don’t pay much attention to it. The fact of the matter, they’re satisfied with the methodologies and constantly review the models.” Twenty percent of the top 30 U.S. insurers, including Allstate, use Colossus today.

Romano isn’t so sure the issue is dead. Insurance is too important to people. He’s seen how it helped make people’s lives a little easier in their time of need. He was proud to call himself an adjuster but knows he lost his way, as has the industry he once so respected. Today, Romano spends his time working on ways to inform consumers about the complexities of insurance, help people the best he can. That’s what he always wanted to do; it’s what insurance is supposed to do. His migraines have all but vanished.

Insurance companies have another controversial black box program that affects what South Carolinians pay for auto and homeowner insurance. Going by “customer rating index” and similar names, these computer models use credit information and other data to estimate whether you are more likely to file a claim. Insurers then use these scores to decide whether to hike or lower your premiums — or deny you coverage altogether.

Insurance companies guard these formulas aggressively, so consumers and even regulators have little idea whether they’re being applied fairly.The Post and Courier, for instance, recently asked the state Department of Insurance for “scoring manuals,” citing the Freedom of Information Act. The insurance department then notified State Farm, Nationwide and Allstate about the request and asked for their comments. Insurers demanded that the material not be released, according to emails obtained by the newspaper.

“This information is proprietary to State Farm and contains commercially valuable trade secret information that State Farm has collected and created and to which State Farm strictly controls access on a need to know basis,” a State Farm official wrote in one email. “It is understood that absent court order the Department will not release the information produced.”

The state Department of Insurance denied the newspaper’s request, even though other states have released these manuals to consumer groups, including the publishers of Consumer Reports. (The newspaper is appealing the department’s determination that the information is confidential.)

The result of this secrecy is that consumers have no way of knowing how their credit scores affect their insurance rates. What’s clear, however, is that the issue continues to generate controversy.

Insurers cite studies that show people with poor credit histories are more likely to file claims. But many consumer advocates say these scores discriminate against some minority consumers and poor people who otherwise might be good insurance risks.

Consumers Union railed against the use of these scores in an extensive study in 2006, saying, “While insurers are preoccupied with gaining a competitive advantage over one another, consumers are getting caught in the crossfire.” Their report found that people could be penalized if they simply opened up several credit card accounts in a year, or made more than two loan inquiries.

Every year, about 47,000 property owners on the coast of South Carolina pay millions of dollars to a special insurance organization that funnels nearly all of this money to a group of super-wealthy companies in Bermuda, Switzerland and other far-flung locales.

Welcome to the Byzantine world of the “wind pools,” where rates are set high on purpose and insurers spend millions to insure themselves.

Most coastal states have wind pools — government-chartered nonprofits that insure high-risk homes and buildings no private insurance company wants to cover.

And some have become massive enterprises. Florida’s wind pool, Citizens Property Insurance Corp., insures 1.4 million properties and collects $3 billion in premiums a year.

South Carolina’s smaller iteration is the S.C. Wind and Hail Association, which every year collects nearly $100 million in premiums from 46,000 homeowners and 1,000 commercial property owners in two zones near the water.

In Charleston County alone, it insures about 10,000 properties valued at $4 billion. On average, owners shell out about $2,040 for coverage against wind and hail damage. That doesn’t include coverage for fires and flooding, which requires separate polices.

“I’m paying almost $5,000 for all my insurance now,” said George L. Williams, a retired veteran from the Isle of Palms whose home is in one of the wind pool zones. “Really and truly, I would like someone to explain what’s going on with the money.”

Some consumer advocates say wind pools reflect a troubling trend: Private insurance companies are shifting high-risk properties to these groups and keeping “the safest risks for themselves,” a report by the Consumer Federation of America said this year.

“It is akin to solving the health insurance crisis by requiring states to cover sick or terminally ill patients, while the private sector writes coverage for young and healthy consumers,” the report said.

Others say wind pools have helped prevent real-estate meltdowns in hurricane-prone areas by giving homeowners another option to buy wind hazard insurance, even though it’s expensive.

What is clear is that as private companies such as Allstate and State Farm pull out of areas near the ocean, wind pools have emerged as significant players in coastal states such as South Carolina, even though, as Rick Amick, chief financial officer of the S.C. Wind and Hail Association, said, “We like to fly under the radar.”

What are wind pools? The wind pool’s roots stretch back to a double-whammy of fear during the 1960s.

After inner-city riots, insurers grew nervous about covering homes in urban areas. States responded by creating FAIR plans, short for “fair access to insurance requirements,” to cover properties that private insurance companies dropped.

At the same time, insurance companies grew anxious about their potential losses in a hurricane strike. The federal government responded by creating the National Flood Insurance Program in 1968; states followed by forming wind pools.

In 1971, South Carolina lawmakers ordered insurers to set up the S.C. Wind and Hail Association. Only people in specially designated zones near the ocean are eligible for wind pool coverage.

Though created by state statute, the association is run by the insurance industry, including many insurers that are canceling policies. The association’s board comprises 11 insurance company officials, two insurance agents and four consumer representatives.

The association is funded by the premiums it collects from property owners. Much of the legwork with customers is done by traditional insurance agents who last year received $9 million in commissions from the association.

Unlike the federal flood insurance program, the South Carolina wind pool receives no money from taxpayers. In the event of a catastrophe, taxpayers wouldn’t be on the hook for claims.

Its small staff works out of an office in Columbia, and one of its main goals is to provide insurance rates that are so high they don’t compete with traditional insurance companies like State Farm and Allstate.

“We don’t want to push companies out of the market, but we do want to be a safety net,” said Smitty Harrison, the longtime head of the association. “It’s a bizarre business model. We want our competition to take our business.”

Although the wind pool collects $97 million a year from South Carolina property owners, it insures more than $17 billion in property. It has no reserve fund to speak of.

That presents the group with a major problem: If a catastrophic hurricane made a direct hit on Charleston or Myrtle Beach, the group would never have enough to cover losses, Harrison said. For this reason, the wind pool must go outside South Carolina to find ways to pay for a future catastrophe.

And it does this by taking out insurance policies of its own.

Masters of disasterInsurance is about spreading risk, and it has a long tradition. Ancient traders increased their odds of getting materials to destinations by spreading cargoes among different ships and caravans.

Today, a relatively small group of wealthy reinsurance companies across the globe do something similar for insurance companies and groups such as the S.C. Wind and Hail Association. In South Carolina, of the roughly $97 million in premiums that were collected in 2011, about $85 million went toward reinsurance.

The world’s 200 reinsurance companies have become global masters of disasters, taking in vast sums of money in Europe to help insurers in the United States pay for a devastating tornado strike in Oklahoma, or using billions of dollars from insurers in the United States to help pay for losses of a tsunami in Japan.

Every year, these companies collect more than $200 billion in premiums from insurance companies and wind pools.

And the insurance industry is quick to say we would be in trouble without them. After hurricanes Rita and Katrina in 2005, reinsurance companies sent billions of dollars to private insurance companies, which in turn paid homeowners with claims.

According to the reinsurance giant Swiss Re, reinsurance companies were responsible for paying 60 percent of those hurricanes’ claims.

Ten reinsurance companies control three-quarters of the market. Munich Re is the largest with 15 percent, and it is expected to make $3.1 billion in profits this year. Because such a small number of companies are involved, some are concerned about the potential for price fixing.

A European Commission report in 2007 cited this possibility and noted that in some European countries, reinsurance companies may control half the market or more. “In other market sectors, such a concentration of market share would be likely to trigger a monopoly investigation.”

Robert Hunter, a former insurance commissioner from Texas now with the Consumer Federation of America, said reinsurance companies in Florida were charging five times more than what their own actuaries said they needed.

In response, Florida has been building a hurricane catastrophe fund, now at $15 billion, a move that helped homeowners save $20 billion on their policies in recent years. But in South Carolina and many other states, wind pools are at the mercy of whatever the reinsurance industry decides to charge, he said.

Every year, Harrison and other staff members with the S.C. Wind and Hail Association travel to reinsurance meetings in London, Bermuda and other reinsurance hot spots. The wind pool’s job, Harrison said, is to sell these companies on the argument that South Carolina’s coastal homeowners are worth covering and that the state’s wind pool operates in a responsible way.

Harrison said their sales pitches have worked well over the years, even though the reinsurance industry tends to look at state wind pools as bad overall risks.

Of the 99 reinsurance entities the state works with, about 80 have decided to cover potential wind pool losses. That means the wind pool effectively spreads the risk of a devastating hurricane hit to 80 companies. Average premiums have risen only 14 percent since 2007.

David Marlett, chairman of Appalachian State University’s Department of Finance, Banking and Insurance, has studied wind pools throughout the Southeast since 1998.

Other states have set up special catastrophe funds or systems to assess property owners and insurers after a storm. Both approaches have problems. A catastrophe fund could be wiped out quickly in a major storm, and when it comes to assessments, “you’re basically asking people who have just had a major loss to pay more money,” Marlett said.

Reinsurance may be expensive, but it takes care of the problem of covering high-risk properties, he said, adding that Harrison and his team have an excellent reputation in the industry.

“I’m comfortable saying that over that time period, the South Carolina wind pool has been one of the best, if not the best, managed residual market program in the country.”

That’s small comfort, however, to customers in wind pool zones who have seen their rates skyrocket — people like Susan and John Watkins.

The couple has lived off Camp Road on James Island for 37 years. In 1989 they stayed in their house during Hurricane Hugo and lost only 12 pine trees and a corner of their roof. They had insurance with State Farm then, and switched to S.C. Farm Bureau when they refinanced.

“In 2007, all of a sudden they dropped our wind and hail coverage,” Susan Watkins said. “They said it was because of increased hurricanes and something called reinsurance.” Like others who have been dropped, she felt betrayed.

“It’s like they’re really into risk avoidance instead of risk insurance.” She called the Department of Insurance. “They were not very nice,” she said. “All they told us was that we would have to get insurance from the wind pool.”

Her last bill from the S.C. Wind and Hail Association was $3,200, and that didn’t include coverage for floods and other hazards.

“It got to the point where it was ridiculous,” she said. She and her husband recently found a private insurance company willing to write a policy for about $2,800. But the high rates are still tough to swallow for retirees. “It’s just killing us, and being in the wind pool zone puts a stigma on us when we have to sell our property,” she said.

In a sense, though, their experience is a wind pool success story.

Staff members with the S.C. Wind and Hail Association want private insurance companies to take business away from them.

“We are truly trying to remain a market of last resort,” Amick said. At the same time, they’re trying not to create too heavy a burden for homeowners.

They acknowledge that setting rates is a bit of an art form. If the wind pool gets a huge influx of homeowners seeking policies, that usually means the group’s rates are too low, said David Leadbitter, chief operating officer. If rates are too high, homeowners complain.

“No computer can figure this out, but if you screw it up, you know the effects immediately,” he said.

One sign that the market has stabilized is that the number of policies has stayed around 47,000 for several years.

The problem homeowners face is that rates are likely to continue going up because reinsurance companies are reassessing their vulnerabilities to disasters, Leadbitter and other experts say.

That’s because insurance industry computer models are predicting higher losses.

The models, dubbed “black boxes” because of their secret algorithms, have their critics, including some who say they overstate the risks and make it easier for insurers and reinsurers to charge higher rates.

Karen Clark, the architect of the first catastrophe computer model, said she found new models have overestimated losses by as much as $53 billion.

A Post and Courier report this month found that South Carolina regulators have little knowledge about the inner-workings of these models and whether they properly assess risk in South Carolina. Other states have found major flaws in models when they looked at them.

Meanwhile, as South Carolina heads into the heart of another hurricane season, homeowners in coastal areas remain in precarious positions.

Their rates are subject to reinsurance giants oceans away; state lawmakers are doing little to support efforts to monitor the fairness of rates; and if their insurance company drops them they’re left with what officials from the wind pool acknowledge is an unusual sales pitch: “We’re not only expensive,” Amick said. “But you get less coverage for your money.”

This component will be re-posted as the new pulitzer.org continues to evolve.