ProPublica, by Jesse Eisinger and Jake Bernstein

Lee C. Bollinger, President of Columbia University (left), presents the 2011 National Reporting prize to Jesse Eisinger (center) and Jake Bernstein (right) of ProPublica.

Winning Work

By Jesse Eisinger and Jake Bernstein

A hedge fund, Magnetar, helped create arcane mortgage-based instruments, pushed for risky things to go inside them and then bet against the investments. (Ethan Miller/Getty Images)

In late 2005, the booming U.S. housing market seemed to be slowing. The Federal Reserve had begun raising interest rates. Subprime mortgage company shares were falling. Investors began to balk at buying complex mortgage securities. The housing bubble, which had propelled a historic growth in home prices, seemed poised to deflate. And if it had, the great financial crisis of 2008, which produced the Great Recession of 2008-09, might have come sooner and been less severe.

At just that moment, a few savvy financial engineers at a suburban Chicago hedge fund helped revive the Wall Street money machine, spawning billions of dollars of securities ultimately backed by home mortgages.

When the crash came, nearly all of these securities became worthless, a loss of an estimated $40 billion paid by investors, the investment banks who helped bring them into the world, and, eventually, American taxpayers.

Yet the hedge fund, named Magnetar for the super-magnetic field created by the last moments of a dying star, earned outsized returns in the year the financial crisis began.

How Magnetar pulled this off is one of the untold stories of the meltdown. Only a small group of Wall Street insiders was privy to what became known as the Magnetar Trade. Nearly all of those approached by ProPublica declined to talk on the record, fearing their careers would be hurt if they spoke publicly. But interviews with participants, e-mails, thousands of pages of documents and details about the securities that until now have not been publicly disclosed shed light on an arcane, secretive corner of Wall Street.

According to bankers and others involved, the Magnetar Trade worked this way: The hedge fund bought the riskiest portion of a kind of securities known as collateralized debt obligations -- CDOs. If housing prices kept rising, this would provide a solid return for many years. But that's not what hedge funds are after. They want outsized gains, the sooner the better, and Magnetar set itself up for a huge win: It placed bets that portions of its own deals would fail.

Along the way, it did something to enhance the chances of that happening, according to several people with direct knowledge of the deals. They say Magnetar pressed to include riskier assets in their CDOs that would make the investments more vulnerable to failure. The hedge fund acknowledges it bet against its own deals but says the majority of its short positions, as they are known on Wall Street, involved similar CDOs that it did not own. Magnetar says it never selected the assets that went into its CDOs.

Magnetar says it was "market neutral," meaning it would make money whether housing rose or fell. (Read their full statement.) Dozens of Wall Street professionals, including many who had direct dealings with Magnetar, are skeptical of that assertion. They understood the Magnetar Trade as a bet against the subprime mortgage securities market. Why else, they ask, would a hedge fund sponsor tens of billions of dollars of new CDOs at a time of rising uncertainty about housing?

Key details of the Magnetar Trade remain shrouded in secrecy and the fund declined to respond to most of our questions. Magnetar invested in 30 CDOs from the spring of 2006 to the summer of 2007, though it declined to name them. ProPublica has identified 26.

An independent analysis commissioned by ProPublica shows that these deals defaulted faster and at a higher rate compared to other similar CDOs. According to the analysis, 96 percent of the Magnetar deals were in default by the end of 2008, compared with 68 percent for comparable CDOs. The study was conducted by PF2 Securities Evaluations, a CDO valuation firm. (Magnetar says defaults don't necessarily indicate the quality of the underlying CDO assets.)

From what we've learned, there was nothing illegal in what Magnetar did; it was playing by the rules in place at the time. And the hedge fund didn't cause the housing bubble or the financial crisis. But the Magnetar Trade does illustrate the perverse incentives and reckless behavior that characterized the last days of the boom.

Magnetar says it invested in 30 CDOs from the spring of 2006 to the summer of 2007. At least nine banks helped the hedge fund hatch these deals, and Merrill Lynch, UBS and Citi all did multiple deals. (From left: Daniel Barry/Getty Images; Jonathan Fickies/Bloomberg News; Seokyong Lee/Bloomberg News)

At least nine banks helped Magnetar hatch deals. Merrill Lynch, Citigroup and UBS all did multiple deals with Magnetar. JPMorgan Chase, often lauded for having avoided the worst of the CDO craze, actually ended up doing one of the riskiest deals with Magnetar, in May 2007, nearly a year after housing prices started to decline. According to marketing material and prospectuses, the banks didn't disclose to CDO investors the role Magnetar played.

Many of the bankers who worked on these deals personally benefited, earning millions in annual bonuses. The banks booked profits at the outset. But those gains were fleeting. As it turned out, the banks that assembled and marketed the Magnetar CDOs had trouble selling them. And when the crash came, they were among the biggest losers.

Some bankers involved in the Magnetar Trade now regret what they did. We showed one of the many people fired as a result of the CDO collapse a list of unusually risky mortgage bonds included in a Magnetar deal he had worked on. The deal was a disaster. He shook his head at being reminded of the details and said: "After looking at this, I deserved to lose my job."

Magnetar wasn't the only market player to come up with clever ways to bet against housing. Many articles and books, including a bestseller by Michael Lewis, have recounted how a few investors saw trouble coming and bet big. Such short bets can be helpful; they can serve as a counterweight to manias and keep bubbles from expanding.

Magnetar's approach had the opposite effect -- by helping create investments it also bet against, the hedge fund was actually fueling the market. Magnetar wasn't alone in that: A few other hedge funds also created CDOs they bet against. And, as the New York Times has reported, Goldman Sachs did too. But Magnetar industrialized the process, creating more and bigger CDOs.

Several journalists have alluded to the Magnetar Trade in recent years, but until now none has assembled a full narrative. Yves Smith, a prominent financial blogger who has reported on aspects of the Magnetar Trade, writes in her new book, "Econned," that "Magnetar went into the business of creating subprime CDOs on an unheard of scale. If the world had been spared their cunning, the insanity of 2006-2007 would have been less extreme and the unwinding milder."

Magnetar Gets Started

Magentar founder Alec Litowitz speaks at a private equity conference held at Kellogg School of Management at Northwestern University in February 2007. (Nathan Mandell)

The guiding force behind Magnetar was Alec Litowitz, a triathlete, astronomy buff and rising star in the investing world. In 2003, Litowitz retired from a Chicago-based hedge fund, Citadel, one of the most successful in the world, where he had spent most of his career and became a top executive. He promised to stay out of the business for two years.

As he waited for his non-compete agreement to expire, Litowitz and his wife traveled through Europe collecting antiques to stock a big house they were building on the shores of Lake Michigan.

By spring 2005, Litowitz's wait was over. Then 38 years old, Litowitz quickly raised money to start his own hedge fund. The fund, Magnetar, attracted $1.7 billion from investors and opened in April.

Litowitz, who declined to be interviewed, had an approach to investing that emphasized scale and simplicity. He told those he hired: "Figure out a way to make money and figure out how to repeat it and do it over and over again," according to a former employee. The firm handed out T-shirts emblazoned with a confident slogan: "Very Bright, Very Magnetic." Employees privately joked about working for a fund named after something like a black hole.

Litowitz brought on board David Snyderman. A New Yorker with a serious mien, Snyderman, in his mid-30s, began hunting for investment opportunities in Wall Street's burgeoning market in mortgage-backed securities.

It didn't take them long to find something promising.

Snyderman and Magnetar focused on Wall Street's mortgage assembly line, which had been super-charged during Litowitz's time away from the business. Banks bundled pools of mortgages into large bonds, which they combined to create even larger investments. These were the now-infamous collateralized debt obligations. Each month, homeowners paid their mortgages. Each month, payments flowed to investors. (Here is an excellent video explaining CDOs.)

Large investors across the globe snapped up the CDOs, which took the hottest investment around -- the U.S. housing market -- and transformed it into something that supposedly had little or no risk. Wall Street preached that the risk had been diluted because it was spread out over such large collections of mortgage bonds. (CDOs can also be based on side bets that rise and fall with the value of other mortgage bonds. These are known as "synthetic" CDOs. Magnetar’s deals were largely synthetic.)

Just as they did with mortgage-backed securities, investment banks divided CDOs into different layers, called tranches. As the mortgages were paid, money flowed to investors holding the top tranche. Since they were the first to get paid, and thus took the least amount of risk, they earned low interest rates. Next came the middle levels -- the so-called mezzanine tranches.

Last in line for money were investors in what's known as the equity. In return for being at the bottom, equity investors got the highest returns, sometimes 20 percent interest -- money they would receive only as long as the vast majority of mortgage holders made their payments.

Even back then, Wall Street insiders called the equity "toxic waste," and as anxiety built in late 2005 that the housing boom was over, investment banks struggled to find takers.

To Magnetar, the toxic waste was an opportunity.

At a time when fewer investors were stepping up to buy equity, the little-known hedge fund put out the word that it wanted lots and lots of it. Magnetar concentrated in a particularly risky corner of the CDO world: deals that were made up of the middle, or mezzanine, slice of subprime mortgage-backed bonds. Magnetar CDOs were big, averaging $1.5 billion, about three times the size of earlier deals built on subprime mortgages.

Magnetar's purchases solved a crucial problem for the banks. Since the equity was so risky and thus difficult to sell, banks didn't like to create new CDOs unless someone committed to buy them. Indeed, such buyers were so crucial that Wall Street referred to them as the CDOs' "sponsors."

Without sponsors, Wall Street's mortgage bond assembly line could grind to a halt, and with it bank profits and banker bonuses. A top CDO banker could earn $3 million to $4 million annually on the CDOs he created and sold.

Usually, investment banks had to go out and find buyers of the equity. With Magnetar, the buyer came right to the bank's doorstep. Wall Street was overjoyed.

"It seemed like a miracle," says one mortgage market investment banker, because "no one" had been buying equity.

"By the end of 2005, the general sense was that the CDO market would slow down. These trades continued to fuel the fire," says Bill Tomljanovic, who worked for a firm that helped build a Magnetar CDO. Magnetar was "a driving force in the market."

According to JPMorgan data, Magnetar's deals amounted to somewhere between a third and half the total volume in the particularly risky corner of the subprime market on which the fund focused.

Outsiders thought Magnetar was piling in at exactly the wrong time. A March 2007 Business Week article titled "Who Will Get Shredded?" would later put Magnetar near the top of its list. The hedge fund, said the magazine, "showed bad timing."

How could Magnetar hope to make money on such risky stuff? It had a second bet that was known only to insiders.

At the same time it was investing in the equity, the fund placed bets that many of the same CDOs it had helped create would actually blow up. It did that using one of the most opaque corners of the investment world: credit default swaps, which function as a kind of insurance on CDOs and other types of bonds.

Credit default swaps work roughly like an insurance policy: You pay a small premium regularly, on any bond you want -- whether you own it or not -- and if it goes bust, you get paid off in full.

Nobody but Magnetar knows the full extent of its bets. Hedge funds are private and they don't disclose the details of their trades. Also, credit default swaps are mostly unregulated and not publicly disclosed. Magnetar says it didn't bet only against its own CDOs. The majority of its credit default swaps, says Magnetar, were on other CDOs. (Update April, 9:We have added additional detail from Magnetar’s response in which the hedge fund says it was “net long” on its own CDOs, an assertion on which the fund has declined to elaborate.)

Since it was the sponsor, Magnetar had privileges. Placing the risky equity was so important to banks that they typically gave those who bought it a say in how the deal was structured. Like all investors, equity buyers had to weigh risk and reward, the goal being to maximize returns while minimizing the chances that your investment will blow up.

But people involved in Magnetar's deals say the hedge fund took a different tack, pushing for riskier bonds to go inside its CDOs. Doing that would make it more likely that Magnetar's bets against the CDO would pay off.

The equity bought by Magnetar represented just a tiny fraction of the overall CDO. If it costs, say, $50 million, an entire CDO could be 20 times that, $1 billion. And if the CDO begins to go south and you're smart enough to have taken out enough insurance, you can make hundreds of millions of dollars. That, of course, would take a bit of the sting out of losing your original $50 million investment in the equity.

Magnetar Does Its First Deal

As Magnetar set up its CDO shop, the hedge fund hired Jim Prusko, a smart and affable investor who had worked previously at the Boston money-manager Putnam Investments. He would shoulder much of the work of courting Wall Street bankers and managers who worked with the hedge fund. He operated out of Magnetar's office in midtown Manhattan around the corner from Saks Fifth Avenue. In an office of 20-somethings, Prusko, then 40 years old, stood out as the "old man."

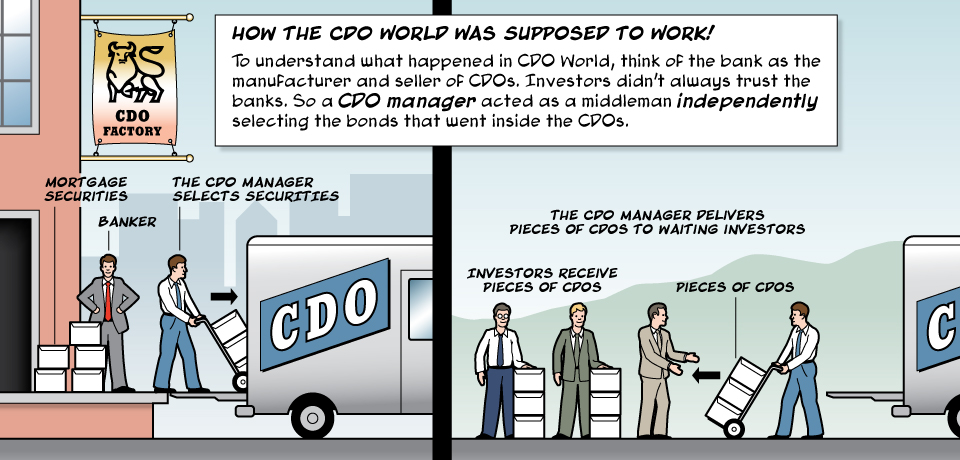

Prusko and his boss at Magnetar, Snyderman, began approaching investment banks, offering to buy the riskiest, highest-yielding portion of CDOs. They always wanted a middleman, known as a CDO manager, on their deals. Many CDOs are operated day to day by such independent firms, who are often brought in by investment banks.

The managers also played a vital role in creating deals. When an investment bank created a CDO, it would often give what amounted to blueprints to the managers, who would then go out and find the exact bundles of bonds to fill the CDO. The managers had a fiduciary duty to represent the CDO fairly to all investors, ensuring investors got accurate and equal information.

Magnetar's deals were numerous and big, and just like for investment banks, the bigger the deal, the larger the fee for managers.

"Prusko's job was to butter up the CDO managers and the bankers," said one banker who dealt with him.

By relying on a manager rather than managing the deal itself, Magnetar had no legal obligations to the CDO or others who bought it.

A guard stands outside the New York headquarters of Deutsche Bank in Lower Manhattan on April 8, 2010. An internal investment fund within Deutsche Bank bought the risky equity along with Magnetar in the hedge fund's maiden CDO.

Magnetar completed its first deal in May 2006. In what became a habit, it named the CDO after a constellation, in this case, "Orion," known for the trio of stars that form the mythological Greek hunter's belt. For its maiden CDO, Magnetar enlisted a partner to buy risky equity alongside it, an internal investment fund within Deutsche Bank.

Deutsche and Magnetar didn't reach for a Wall Street powerhouse to put the deal together. Instead the investors worked with Alex Rekeda, a young Ukrainian immigrant who was then working for Calyon, the investment banking arm of the French bank Crédit Agricole.

Magnetar and Deutsche were deeply involved in creating Orion. "We want to make sure we control the deal," a banker who worked on it recalls them emphasizing.

One person involved in Orion recalls Deutsche's point person, Michael Henriques, and Magnetar's Prusko pressuring the CDO manager, a division of the Dutch bank NIBC, to include specific lists of bonds in the deal.

Prusko and Henriques told this person that the investors "needed more spread in the portfolio." More "spread" means more return and more risk.

This person recalled Magnetar asking, "Would you consider these bonds?" Their suggestions were invariably for riskier bonds. "Let's just say we didn't think their suggestions made a lot of sense," the person said.

He said the CDO manager refused Magnetar's requests to put riskier bonds in the deal. Still, it was an eye-opening experience. "I began to realize there were things you had to defend yourself against," he said.

Magnetar and Deutsche declined to comment on Orion specifically. Magnetar says it made suggestions about the general outlines of the CDOs. But, the hedge fund says, it "did not select the underlying assets of the CDO at any time prior to or subsequent to transaction issuance."

Other buyers of the CDO could have figured out they were getting relatively risky bonds, but they would have had to look hard at the minutiae of the deal. By this point in market history, the ratings had less and less meaning. Two sets of bonds rated AA could have very different levels of risk. Most investors chose not to dig too deeply.

One investor in Orion was a fund affiliated with IKB, a small German bank. Eventually, it invested in at least four more Magnetar deals. In mid-2007, because of the disastrous investments in subprime securities, the German government was forced to bail out IKB. The failure of the bank was an early warning sign of the global financial crisis.

Deutsche's Henriques would later quit the bank and join Magnetar.

Orion lost value but never defaulted. That was better than every subsequent CDO that Magnetar helped create, according to ProPublica's research.

Magnetar's (Nearly) Perpetual Money Machine

By buying the risky bottom slices of CDOs, Magnetar didn't just help create more CDOs it could bet against. Since it owned a small slice of the CDO, Magnetar also received regular payments as its investments threw off income.

With this, Magnetar solved a conundrum of those who bet against the market. An investor might be confident that things are heading south, but not know when. While the investor waits, it costs money to keep the bet going. Many a short seller has run out of cash at the gates of a big payday.

Magnetar could keep money flowing -- via its small investments in CDOs -- and could use that money to pay for its bets against CDOs.

Similar, commonly traded, assets appeared in multiple Magnetar CDOs. Experts say the benefit of that overlap to Magnetar was that when the hedge fund bet against non-Magnetar CDOs, the CDOs still had similar characteristics to the ones Magnetar had invested in.

Soon enough, bankers and CDO managers had a sense of how it worked. "Everyone knew," said one person who managed Magnetar CDOs. "They used the equity to fund the shorts."

Magnetar further increased its odds by insisting that the CDOs it helped create had an unusual construction. Typically, cash flowing to the last-in-line equity buyers is cut off at the first signs of trouble -- such as a rise in mortgage delinquencies. Those at the top of the CDO -- who accepted lower returns for less risk -- received that cash, leaving none for the high-risk holders.

Magnetar wanted its deals to be "triggerless," meaning lacking these cash-flow dams. When the market turned shaky and homeowners began to default, money kept flowing down to the risky slices that Magnetar owned.

Even today, bankers and managers speak with awe at the elegance of the Magnetar Trade. Others have become famous for betting big against the housing market. But they had taken enormous risks. Meanwhile, Magnetar had created a largely self-funding bet against the market.

E-mails Give Glimpse of How Magnetar Worked

By the fall of 2006, housing prices had already peaked and Magnetar's assembly line started producing, helping to create CDOs it would bet against. The hedge fund's appetite seemed insatiable. The deals were the talk of CDO desks across Wall Street.

Between the end of September and the middle of December 2006, Magnetar had a hand in spawning at least 15 CDOs, worth an estimated $23 billion. Among the banks involved with those deals were Citigroup, Lehman Brothers and Merrill Lynch.

E-mails obtained by ProPublica from that time suggest Magnetar's clout. The firm was involved at the start of deals and pushed for riskier bonds to be included.

After Magnetar expressed interest in buying the equity, the French bank Société Générale began to build the CDO, and selected a New York-based manager, Ischus Capital Management, which would choose the exact bonds to go into the CDO.

Magnetar wanted to name the CDO after a small constellation in the southern sky called Hydrus, which means "male water snake." But by late September, Magnetar and Ischus began sparring over the composition of the deal.

Magnetar pressed Ischus to buy lower-quality assets for the deal, according to three people familiar with Hydrus. In an e-mail to bankers at Société Générale and Ischus executives, Magnetar's CDO specialist, Jim Prusko, wrote on Sept. 29, 2006, "The original portfolio target spreadsheet that I have... had a strangely low spread target. That of course would not at all be beneficial to us. I have attached the target portfolio that I would like for this deal with target spreads."

The portfolio Magnetar outlined didn't list specific bonds, but executives at the CDO manager Ischus felt that they understood what Prusko wanted. A request for higher-spreading assets means more risk in the deal.

Andrew Shook, an Ischus executive, answered forcefully on Oct. 3, "We will not assemble a portfolio we are not proud of and feel strongly about in the name of a spread target."

Prusko dialed down the pressure, responding within an hour. "Of course, the actual security selection is totally your purview," he wrote. "I just wanted to make sure the overall portfolio characteristics worked for our strategy."

Shook declined to comment on the e-mail exchange. Magnetar says that the deal as originally conceived wouldn't have been profitable and that it was merely trying to get a higher return -- a higher "spread" -- to balance out the risk it was taking in owning the bottom-rated slice of the CDO.

The two sides subsequently drifted apart, partly over Ischus's unease with Magnetar's pressure, and the deal was never completed.

Concerns About 'Reputational Risks'

As part of the big business Magnetar was doing in the fall of 2006, the hedge fund put together a CDO with Lehman Brothers named for the constellation Libra. John Mawe, a banker who worked on Libra, remembers that "there was a back-and-forth fight" about the assets between the bank's CDO manager and Magnetar, with the hedge fund pushing for riskier assets.

Mawe says Lehman's CDO in-house-management arm, which handled the deal, never put assets into Libra that it thought were bad investments.

Among the other banks that Magnetar approached during that time was Deutsche Bank, with whom it had teamed up to do its first deal months earlier. Deutsche Bank was anxious for business in order to maintain its standing as one of the top CDO banks, according to one of its bankers. Deutsche recommended CDO manager State Street Global Advisors.

The State Street managers were "highly skeptical" of doing a deal with Magnetar, according to one participant. "State Street wanted their deals to do well," said the participant, and with Magnetar, there was "a lot of reputational risk to be concerned about."

Hoping to close the deal, Magnetar's master salesman Jim Prusko drove up from his home in the New York suburbs to State Street's headquarters in Boston, to mollify executives in the management team. After the meeting, the deal went forward. As one banker explained, "there were other managers who were dying to do this deal" and get the millions in fees.

After subprime losses, State Street closed the business that managed its CDOs in late 2007. Frank Gianatasio, who worked in State Street's CDO business says, "We were comfortable with every transaction we put into our CDOs."

Deutsche, Magnetar and State Street called the $1.6 billion CDO they created Carina, a constellation whose name in Latin means a ship's keel. In November 2007, Carina had the distinction of being the first subprime CDO of its kind to be forced into liquidation.

State Street and Magnetar declined to comment on their negotiations over Carina.

A Lawsuit Suggests Merrill Lynch's Role

By early 2007, the mortgage market was falling apart. Lenders were reporting big losses, delinquencies were mounting -- and Magnetar's business was booming.

Between late February and April, banks rolled out five Magnetar-sponsored deals, with a value of about $7.2 billion. Among them was a $1.5 billion CDO named Norma. Following Magnetar's branding convention, Norma is a constellation in the Southern Hemisphere named for the Latin word for "normal." This CDO was anything but.

Details about Norma, which was created by Merrill Lynch, have emerged through an ongoing lawsuit between Merrill and Dutch bank Cooperatieve Centrale Raiffeisen-Boerenleenbank, known commonly on Wall Street as Rabobank. (The Wall Street Journal had the first detailed report of Norma, in late 2007.) The dispute involves a side transaction that Rabobank made with Merrill involving Norma. Magnetar is not a party to the litigation. Yet the allegations are scathing in their depiction of how the CDO was developed.

"Merrill Lynch teamed up with one of its most prized hedge fund clients -- an infamous short seller that had helped Merrill Lynch create four other CDOs -- to create Norma as a tailor-made way to bet against the mortgage-backed securities market," the complaint reads. (Emphasis in the original.)

"[T]o facilitate the selection of assets that would allow Norma to operate as a hedging instrument rather than an investment vehicle, Merrill Lynch hand-picked a beholden collateral manager that was willing to ignore its fiduciary duties to Norma's investors."

The manager for Norma was a small shop out of Long Island, N.Y., called NIR Capital Management. Run by Corey Ribotsky, the firm's primary line of business before entering CDOs was speculating in penny stocks.

NIR brought in a team of experienced bankers to run its CDO business. The firm also had a variety of other ventures. At one point, they put money into a documentary called "American Cannibal," that profiled the aborted launch of a reality television show in which contestant were stranded on an island and goaded into cannibalism. (The New York Times found it "absorbing.") Ribotsky is now under investigation by federal authorities for misleading clients about its investment returns. NIR and Merrill Lynch declined to comment on dealings with Magnetar; Merrill Lynch denies liability in the litigation. Magnetar declined to comment.

Norma began to suffer setbacks even before the deal closed in March 2007. According to the lawsuit, by the time Norma was completed, its value had already declined by more than 20 percent.

JPMorgan Gets Into the Game -- And Loses

Despite the bad news in the mortgage market, Magnetar continued to find a few willing bankers to do CDOs, including a new one: JPMorgan Chase.

JPMorgan had avoided many of the complex financial transactions that decimated the banking industry. As the market grew frothier, JPMorgan pulled back from the CDO business. In 2005, the men who ran JPMorgan's CDO unit told their bosses that they couldn't see how to complete a CDO without sticking the bank with the large top tier, which would not appeal to investors because of its low returns. Other banks dealt with this problem by retaining these CDO layers on their books.

But by mid-2006, JPMorgan joined the herd. It hired bankers to expand its CDO team and got to work.

A few months later -- in early 2007 -- Magnetar and JPMorgan banged out a deal. Unlike the earlier CDOs Magnetar helped create, this one wasn't named after a constellation. Instead, the deal was called “Squared,” after the term for a CDO that was made up of other CDOs. Squared was filled in part with other CDOs Magnetar had helped create.

According to a person familiar with how the deal came together, Magnetar committed to purchase $10 million worth of Squared's equity. Magnetar's purchase allowed JPMorgan to create and sell a $1.1 billion CDO. As it had on previous deals, Magnetar pushed the bankers to select riskier bonds. "They really cared about it," said the person involved in the deal. "They wouldn't pull punches. It was always going to be crappier."

The hedge fund requested that Squared have slices from many Magnetar CDOs, including Auriga, Carina, Libra, Pyxis and Virgo. They all went into the deal. Magnetar also successfully pushed for Squared to include slices from one of the Abacus deals, a group of CDOs that, as the New York Times later reported, Goldman Sachs had created and bet against.

JPMorgan earned $20 million in creating Squared, according to the person involved in the deal.

JPMorgan's sales force fanned out across the globe. It sold parts of the CDO to 17 institutional investors, according to a person familiar with the transaction. The deal closed in May 2007, nearly a year after housing prices had peaked. Within eight months, Squared dropped to a fraction of its initial value.

Just about everybody lost out, including Thrivent Financial for Lutherans, a Minnesota-based not-for-profit fraternal organization, whose $10 million investment was wiped out. Thrivent declined to comment.

Small pieces of Squared, as well as Magnetar's CDO Norma, also ended up in mutual funds run by Morgan Keegan, a regional investment bank based in Memphis, Tenn.

The funds, advertised as conservative investments, cratered after betting on various exotic assets. Morgan Keegan was sued by individual investors who claimed that they were misled about the risks. Among the investors was former Chicago Bulls player Horace Grant, who was awarded $1.4 million in arbitration. This week, the SEC accused two Morgan Keegan employees of misleading fund investors about the value of its holdings in CDOs. Morgan Keegan called the charges "factually inaccurate" and promised to defend itself "vigorously." Morgan Keegan did not respond to a request for comment on the specifics of the two Magnetar CDOs.

The biggest loser was JPMorgan Chase itself, which had kept the large, supposedly safe top slices of Squared on its books, without hedging itself. The bank lost about $880 million on the CDO. JPMorgan declined to comment on the details of the transaction.

Magnetar came out a winner. The fund earned about $290 million on its bet against Squared, according to a person familiar with the deal. Magnetar declined to comment.

Magnetar's Exit: A Deal so Bad Even a Credit-rating Agency Balked

Prusko was buoyant as Magnetar's trades began to make money as its short bets rose in value. One friend recalls Prusko ribbing him: "What are you going to do after this blows up?" (Magnetar declined to comment on the exchange.)

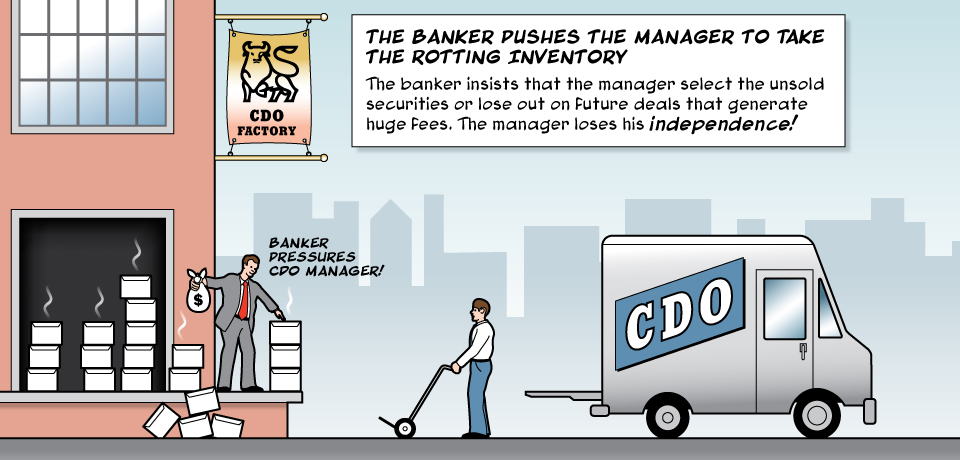

In the spring of 2007, Magnetar began to have a problem: The hedge fund was sitting on hundreds of millions of dollars' worth of CDO equity and other low-rated portions of its deals. With the decline of housing prices accelerating, off-loading these pieces would be very hard.

Magnetar needed a buyer and some deft financial engineering. It found the answer through its former partner, Alex Rekeda, who had been the banker on Magnetar's first CDO. Rekeda now worked at Mizuho, one of Japan's biggest banks. Mizuho was eager to get into the CDO world. It hired Rekeda in part because he could bring Magnetar's business, according to one CDO manager who worked with him.

Rekeda and Magnetar came up with a remarkable CDO. They took their risky portions of 18 CDOs they had helped created -- and repackaged them to sell them to others. Bundling up the dregs of a CDO was rare, if not unprecedented.

This deal, Tigris, which closed in March 2007, tied together $902 million of Magnetar's risky assets. Rekeda convinced two rating agencies, Standard & Poor's and Fitch, to rate it. Fitch designated $259 million of it as triple A, the highest rating. S&P rated nearly $501 million as triple A. (When contacted for this article, S&P said it was comfortable rating Tigris; Fitch didn't respond to questions about the deal.)

In a highly unusual move, the third major rating agency, Moody's, refused to rate Tigris. Rekeda lobbied Moody's for a rating, according to a person familiar with the deal. But Moody's then-head of CDOs, Eric Kolchinsky, wouldn't budge.

Magnetar got $450 million from Mizuho, which in return received income from assets in Tigris, according to several people familiar with the transaction. It was what's known as a non-recourse loan: If things went wrong, Mizuho could only lay claim to what was in Tigris.

In response to ProPublica's questions about this deal, Magnetar said the fund "as a matter of general practice, and as do most hedge funds, enters into non-recourse financing on specific assets in its portfolio."

By September, just six months after Tigris had been created, Fitch downgraded most of the CDO's slices. By the end of January 2008, the CDO had gone into default. The Japanese ended up with the paper, which was worthless. Mizuho eventually wrote Tigris off, as part of about $7 billion in total losses from its subprime missteps. Mizuho declined to comment, as did Magnetar.

Just as with a refi gone bad, when Tigris was wiped out, the hedge fund walked away from the house -- in this case its collateral. A person who worked on Tigris boasted about how innovative the deal was. If it hadn't blown up, he says, it would have been "deal of the year." For Magnetar, it may have been.

Records it shared with investors show Magnetar had a spectacular 2007. Founder Alec Litowitz pulled down $280 million, according to Alpha Magazine. That spring, a trade journal awarded Prusko and Snyderman "Investor of the Year" honors. The Magnetar Constellation Fund, the firm's fund that had the most exposure to the CDO trades, was up 76 percent in 2007, according to a presentation Magnetar gave to investors in early 2009. The main fund, the Magnetar Capital Fund, was up 26 percent that year. By the end of 2007, Magnetar had $7.6 billion under management, up from the $1.7 billion it began with two years earlier. Magnetar declined to comment on its performance.

ProPublica has learned that the SEC has been looking into how the Magnetar deals were created, but it's not clear how much progress the investigation has been made or who might be the target. In a statement yesterday, Magnetar said:

Our understanding is that for some time, the SEC staff has been looking broadly at the sales, marketing, and structuring of CDOs. In connection with that inquiry, the SEC staff has from time to time requested information from Magnetar and other market participants, and Magnetar has been cooperating and responding to the requests. We are not aware that this inquiry is focused on any particular person or firm.

ProPublica Research Director Lisa Schwartz and researcher Kitty Bennett contributed to this story. ProPublica’s Ryan Knutson also helped with research. Finally, a big thanks to This American Life’s Alex Blumberg.

© 2010 ProPublica, Inc.

by Jesse Eisinger and Jake Bernstein

In April, we reported that Magnetar helped spur the creation of at least 30 collateralized debt obligations, worth about $40 billion, as part of a strategy to bet against the mortgage securities market. The fund would purchase the riskiest portion of the deals, enabling the banks to complete the transactions. Magnetar also frequently bet against those same deals, using sidebets. (We detailed Magnetar’s trades in a story in partnership with Chicago Public Radio’s This American Life and NPR’s Planet Money.)

One such deal was Squared, a collateralized debt obligation arranged by J.P. Morgan, completed in May 2007. Having declined to respond to our questions on Squared for our April story, Magnetar now disputes ProPublica’s account of the Squared transaction.

Magnetar gave their response in a Sept. 30 letter, which they sent after receiving questions from ProPublica. We have been reporting on the matter since receiving Magnetar’s letter, and we stand by our account of Magnetar’s role in structuring the transaction.

Magnetar said in its letter that the Squared transaction was initiated by GSC and JP Morgan “independently of Magnetar and well before Magnetar agreed to invest in the equity tranche of Squared.” Magnetar says it wasn’t involved in the naming of the deal. (Read the letter.)

Magnetar also said in its letter that that the fund “did not at any time require or expect any specific assets to be purchased into the Squared transaction.” The fund said GSC, a third-party CDO manager, “at all times exercised its own discretion and judgment regarding the characteristics and appropriateness of each of the assets selected for inclusion in Squared.”

In the original story, ProPublica wrote that the hedge fund “requested that Squared have slices from many Magnetar CDOs, including Auriga, Carina, Libra, Pyxis and Virgo. They all went into the deal.” The story also said Magnetar successfully pushed for Squared to include a slice from one of the Abacus deals, a group of CDOs that Goldman Sachs had created and bet against.

In its letter, the fund says that assets linked to Carina, Libra, Virgo and Abacus were purchased for Squared “prior to Magnetar’s agreeing to purchase equity in Squared.” Though the assets linked to Auriga and Pyxis were selected by GSC after Magnetar agreed to invest in the equity of Squared, they were selected by GSC, acting independently, according to Magnetar.

ProPublica’s original source, a person familiar with the transaction, continues to maintain that Magnetar requested that specific assets go into Squared. This person also says that emails show Magnetar executives discussing specific assets with bankers from JP Morgan.

GSC had been the manager on four previous Magnetar CDOs, in which it had purchased equity. The manager was familiar with the type of collateral that went into Magnetar deals. Because of this, the timing of Magnetar’s agreement to purchase equity in Squared may not be relevant in answering the question of whether it influenced the selection or not.

The original ProPublica story said that “unlike the earlier CDOs it helped create, Magnetar didn't name this one after a constellation. Opting for a more literal name, they called the deal ‘Squared,’ after the term for a CDO that was made up of other CDOs.”

Magnetar’s Sept. 30 response says that the transaction, having been initiated before it agreed to invest in the equity, was already named Squared and that Magnetar “had nothing to do with the naming of Squared.”

We have corrected the story to remove the suggestion that Magnetar named the deal.

By Jake Bernstein and Jesse Eisinger

Over the last two years of the housing bubble, Wall Street bankers perpetrated one of the greatest episodes of self-dealing in financial history.

Faced with increasing difficulty in selling the mortgage-backed securities that had been among their most lucrative products, the banks hit on a solution that preserved their quarterly earnings and huge bonuses:

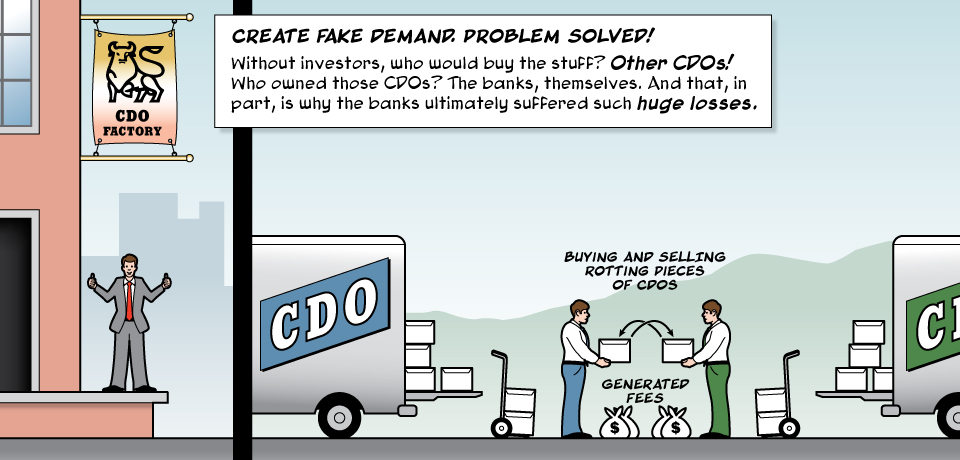

They created fake demand.

A ProPublica analysis shows for the first time the extent to which banks -- primarily Merrill Lynch, but also Citigroup, UBS and others -- bought their own products and cranked up an assembly line that otherwise should have flagged.

The products they were buying and selling were at the heart of the 2008 meltdown -- collections of mortgage bonds known as collateralized debt obligations, or CDOs.

As the housing boom began to slow in mid-2006, investors became skittish about the riskier parts of those investments. So the banks created -- and ultimately provided most of the money for -- new CDOs. Those new CDOs bought the hard-to-sell pieces of the original CDOs. The result was a daisy chain that solved one problem but created another: Each new CDO had its own risky pieces. Banks created yet other CDOs to buy those.

Individual instances of these questionable trades have been reported before, but ProPublica's investigation, done in partnership with NPR's Planet Money, shows that by late 2006 they became a common industry practice.

An analysis by research firm Thetica Systems, commissioned by ProPublica, shows that in the last years of the boom, CDOs had become the dominant purchaser of key, risky parts of other CDOs, largely replacing real investors like pension funds. By 2007, 67 percent of those slices were bought by other CDOs, up from 36 percent just three years earlier. The banks often orchestrated these purchases. In the last two years of the boom, nearly half of all CDOs sponsored by market leader Merrill Lynch bought significant portions of other Merrill CDOs.

ProPublica also found 85 instances during 2006 and 2007 in which two CDOs bought pieces of each other. These trades, which involved $107 billion worth of CDOs, underscore the extent to which the market lacked real buyers. Often the CDOs that swapped purchases closed within days of each other, the analysis shows.

There were supposed to be protections against this sort of abuse. While banks provided the blueprint for the CDOs and marketed them, they typically selected independent managers who chose the specific bonds to go inside them. The managers had a legal obligation to do what was best for the CDO. They were paid by the CDO, not the bank, and were supposed to serve as a bulwark against self-dealing by the banks, which had the fullest understanding of the complex and lightly regulated mortgage bonds.

It rarely worked out that way. The managers were beholden to the banks that sent them the business. On a billion-dollar deal, managers could earn a million dollars in fees, with little risk. Some small firms did several billion dollars of CDOs in a matter of months.

"All these banks for years were spawning trading partners," says a former executive from Financial Guaranty Insurance Company, a major insurer of the CDO market. "You don't have a trading partner? Create one."

The executive, like most of the dozens of people ProPublica spoke with about the inner workings of the market at the time, asked not to be named out of fear of being sucked into ongoing investigations or because they are involved in civil litigation.

Keeping the assembly line going had a wealth of short-term advantages for the banks. Fees rolled in. A typical CDO could net the bank that created it between $5 million and $10 million -- about half of which usually ended up as employee bonuses. Indeed, Wall Street awarded record bonuses in 2006, a hefty chunk of which came from the CDO business.

The self-dealing super-charged the market for CDOs, enticing some less-savvy investors to try their luck. Crucially, such deals maintained the value of mortgage bonds at a time when the lack of buyers should have driven their prices down.

But the strategy of speeding up the assembly line had devastating consequences for homeowners, the banks themselves and, ultimately, the global economy. Because of Wall Street's machinations, more mortgages had been granted to ever-shakier borrowers. The results can now be seen in foreclosed houses across America.

The incestuous trading also made the CDOs more intertwined and thus fragile, accelerating their decline in value that began in the fall of 2007 and deepened over the next year. Most are now worth pennies on the dollar. Nearly half of the nearly trillion dollars in losses to the global banking system came from CDOs, losses ultimately absorbed by taxpayers and investors around the world. The banks' troubles sent the world's economies into a tailspin from which they have yet to recover.

It remains unclear whether any of this violated laws. The SEC has said that it is actively looking at as many as 50 CDO managers as part of its broad examination of the CDO business' role in the financial crisis. In particular, the agency is focusing on the relationship between the banks and the managers. The SEC is exploring how deals were structured, if any quid pro quo arrangements existed, and whether banks pressured managers to take bad assets.

The banks declined to directly address ProPublica's questions. Asked about its relationship with managers and the cross-ownership among its CDOs, Citibank responded with a one-sentence statement:

"It has been widely reported that there are ongoing industry-wide investigations into CDO-related matters and we do not comment on pending investigations."

None of ProPublica's questions had mentioned the SEC or pending investigations.

Posed a similar list of questions, Bank of America, which now owns Merrill Lynch, said:

"These are very specific questions regarding individuals who left Merrill Lynch several years ago and a CDO origination business that, due to market conditions, was discontinued by Merrill before Bank of America acquired the company."

This is the second installment of a ProPublica series about the largely hidden history of the CDO boom and bust. Our first story looked at how one hedge fund helped create at least $40 billion in CDOs as part of a strategy to bet against the market. This story turns the focus on the banks.

Merrill Lynch Pioneers Pervert the Market

By 2004, the housing market was in full swing, and Wall Street bankers flocked to the CDO frenzy. It seemed to be the perfect money machine, and for a time everyone was happy.

Homeowners got easy mortgages. Banks and mortgage companies felt secure lending the money because they could sell the mortgages almost immediately to Wall Street and get back all their cash plus a little extra for their trouble. The investment banks charged massive fees for repackaging the mortgages into fancy financial products. Investors all around the world got to play in the then-phenomenal American housing market.

The mortgages were bundled into bonds, which were in turn combined into CDOs offering varying interest rates and levels of risk.

Investors holding the top tier of a CDO were first in line to get money coming from mortgages. By 2006, some banks often kept this layer, which credit agencies blessed with their highest rating of Triple A.

Buyers of the lower tiers took on more risk and got higher returns. They would be the first to take the hit if homeowners funding the CDO stopped paying their mortgages. (Here's a video explaining how CDOs worked.)

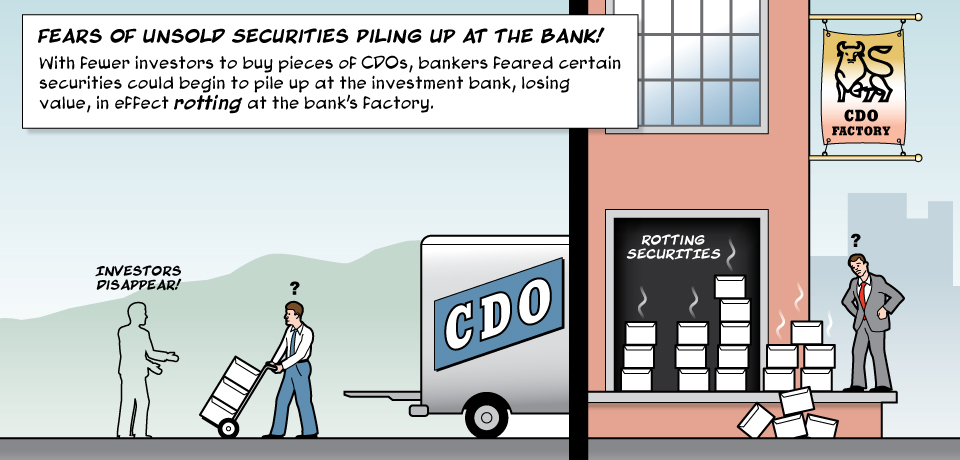

Over time, these risky slices became increasingly hard to sell, posing a problem for the banks. If they remained unsold, the sketchy assets stayed on their books, like rotting inventory. That would require the banks to set aside money to cover any losses. Banks hate doing that because it means the money can't be loaned out or put to other uses.

Being stuck with the risky portions of CDOs would ultimately lower profits and endanger the whole assembly line.

The banks, notably Merrill and Citibank, solved this problem by greatly expanding what had been a common and accepted practice: CDOs buying small pieces of other CDOs.

Architects of CDOs typically included what they called a "bucket" -- which held bits of other CDOs paying higher rates of interest. The idea was to boost overall returns of deals primarily composed of safer assets. In the early days, the bucket was a small portion of an overall CDO.

One pioneer of pushing CDOs to buy CDOs was Merrill Lynch's Chris Ricciardi, who had been brought to the firm in 2003 to take Merrill to the top of the CDO business. According to former colleagues, Ricciardi's team cultivated managers, especially smaller firms.

Merrill exercised its leverage over the managers. A strong relationship with Merrill could be the difference between a business that thrived and one that didn't. The more deals the banks gave a manager, the more money the manager got paid.

As the head of Merrill's CDO business, Ricciardi also wooed managers with golf outings and dinners. One Merrill executive summed up the overall arrangement: "I'm going to make you rich. You just have to be my bitch."

But not all managers went for it.

An executive from Trainer Wortham, a CDO manager, recalls a 2005 conversation with Ricciardi. "I wasn't going to buy other CDOs. Chris said: 'You don't get it. You have got to buy other guys' CDOs to get your deal done. That's how it works.'" When the manager refused, Ricciardi told him, "'That's it. You are not going to get another deal done.'" Trainer Wortham largely withdrew from the market, concerned about the practice and the overheated prices for CDOs.

Ricciardi declined multiple requests to comment.

Merrill CDOs often bought slices of other Merrill deals. This seems to have happened more in the second half of any given year, according to ProPublica's analysis, though the purchases were still a small portion compared to what would come later. Annual bonuses are based on the deals bankers completed by yearend.

Ricciardi left Merrill Lynch in February 2006. But the machine he put into place not only survived his departure, it became a model for competitors.

As Housing Market Wanes, Self-Dealing Takes Off

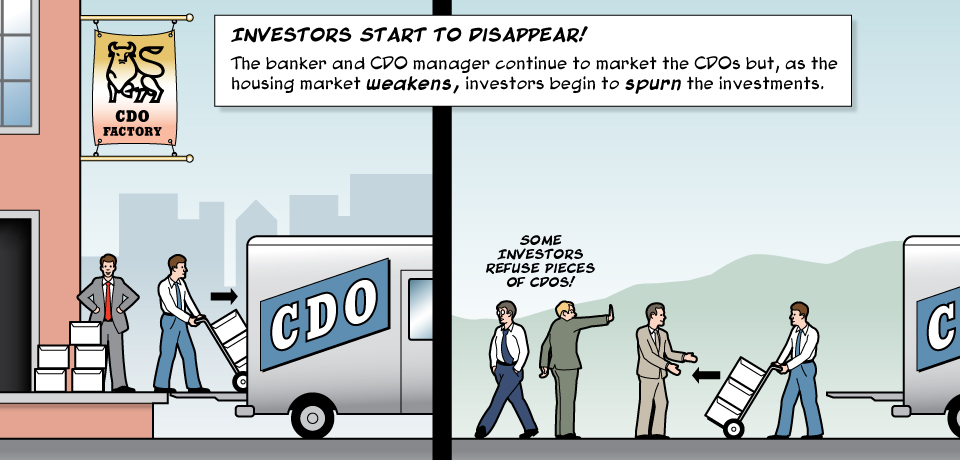

By mid-2006, the housing market was on the wane. This was particularly true for subprime mortgages, which were given to borrowers with spotty credit at higher interest rates. Subprime lenders began to fold, in what would become a mass extinction. In the first half of the year, the percentage of subprime borrowers who didn't even make the first month's mortgage payment tripled from the previous year.

That made CDO investors like pension funds and insurance companies increasingly nervous. If homeowners couldn't make their mortgage payments, then the stream of cash to CDOs would dry up. Real "buyers began to shrivel and shrivel," says Fiachra O'Driscoll, who co-ran Credit Suisse's CDO business from 2003 to 2008.

Faced with disappearing investor demand, bankers could have wound down the lucrative business and moved on. That's the way a market is supposed to work. Demand disappears; supply follows. But bankers were making lots of money. And they had amassed warehouses full of CDOs and other mortgage-based assets whose value was going down.

Rather than stop, bankers at Merrill, Citi, UBS and elsewhere kept making CDOs.

The question was: Who would buy them?

The top 80 percent, the less risky layers or so-called "super senior," were held by the banks themselves. The beauty of owning that supposedly safe top portion was that it required hardly any money be held in reserve.

That left 20 percent, which the banks did not want to keep because it was riskier and required them to set aside reserves to cover any losses. Banks often sold the bottom, riskiest part to hedge funds. That left the middle layer, known on Wall Street as the "mezzanine," which was sold to new CDOs whose top 80 percent was ultimately owned by ... the banks.

"As we got further into 2006, the mezzanine was going into other CDOs," says Credit Suisse's O'Driscoll.

This was the daisy chain. On paper, the risky stuff was gone, held by new independent CDOs. In reality, however, the banks were buying their own otherwise unsellable assets.

How could something so seemingly short-sighted have happened?

It's one of the great mysteries of the crash. Banks have fleets of risk managers to defend against just such reckless behavior. Top executives have maintained that while they suspected that the housing market was cooling, they never imagined the crash. For those doing the deals, the payoff was immediate. The dangers seemed abstract and remote.

The CDO managers played a crucial role. CDOs were so complex that even buyers had a hard time seeing exactly what was in them -- making a neutral third party that much more essential.

"When you're investing in a CDO you are very much putting your faith in the manager," says Peter Nowell, a former London-based investor for the Royal Bank of Scotland. "The manager is choosing all the bonds that go into the CDO." (RBS suffered mightily in the global financial meltdown, posting the largest loss in United Kingdom history, and was de facto nationalized by the British government.)

Source: Asset-Backed Alert

By persuading managers to pick the unsold slices of CDOs, the banks helped keep the market going. "It guaranteed distribution when, quite frankly, there was not a huge market for them," says Nowell.

The counterintuitive result was that even as investors began to vanish, the mortgage CDO market more than doubled from 2005 to 2006, reaching $226 billion, according to the trade publication Asset-Backed Alert.

Citi and Merrill Hand Out Sweetheart Deals

As the CDO market grew, so did the number of CDO management firms, including many small shops that relied on a single bank for most of their business. According to Fitch, the number of CDO managers it rated rose from 89 in July 2006 to 140 in September 2007.

One CDO manager epitomized the devolution of the business, according to numerous industry insiders: a Wall Street veteran named Wing Chau.

Earlier in the decade, Chau had run the CDO department for Maxim Group, a boutique investment firm in New York. Chau had built a profitable business for Maxim based largely on his relationship with Merrill Lynch. In just a few years, Maxim had corralled more than $4 billion worth of assets under management just from Merrill CDOs.

In August 2006, Chau bolted from Maxim to start his own CDO management business, taking several colleagues with him. Chau's departure gave Merrill, the biggest CDO producer, one more avenue for unsold inventory.

Chau named the firm Harding, after the town in New Jersey where he lived. The CDO market was starting its most profitable stretch ever, and Harding would play a big part. In an eleven-month period, ending in August 2007, Harding managed $13 billion of CDOs, including more than $5 billion from Merrill, and another nearly $5 billion from Citigroup. (Chau would later earn a measure of notoriety for a cameo appearance in Michael Lewis' bestseller "The Big Short," where he is depicted as a cheerfully feckless "go-to buyer" for Merrill Lynch's CDO machine.)

Chau had a long-standing friendship with Ken Margolis, who was Merrill's top CDO salesman under Ricciardi. When Ricciardi left Merrill in 2006, Margolis became a co-head of Merrill's CDO group. He carried a genial, let's-just-get-the-deal-done demeanor into his new position. An avid poker player, Margolis told a friend that in a previous job he had stood down a casino owner during a foreclosure negotiation after the owner had threatened to put a fork through his eye.

Chau's close relationship with Merrill continued. In late 2006, Merrill sublet office space to Chau's startup in the Merrill tower in Lower Manhattan's financial district. A Merrill banker, David Moffitt, scheduled visits to Harding for prospective investors in the bank's CDOs. "It was a nice office," overlooking New York Harbor, recalls a CDO buyer. "But it did feel a little weird that it was Merrill's building," he said.

Moffitt did not respond to requests for comment.

Under Margolis, other small managers with meager track records were also suddenly handling CDOs valued at as much as $2 billion. Margolis declined to answer any questions about his own involvement in these matters.

A Wall Street Journal article ($) from late 2007, one of the first of its kind, described how Margolis worked with one inexperienced CDO manager called NIR on a CDO named Norma, in the spring of that year. The Long Island-based NIR made about $1.5 million a year for managing Norma, a CDO that imploded.

"NIR's collateral management business had arisen from efforts by Merrill Lynch to assemble a stable of captive small firms to manage its CDOs that would be beholden to Merrill Lynch on account of the business it funneled to them," alleged a lawsuit filed in New York state court against Merrill over Norma that was settled quietly after the plaintiffs received internal Merrill documents.

NIR declined to comment.

Banks had a variety of ways to influence managers' behavior.

Some of the few outside investors remaining in the market believed that the manager would do a better job if he owned a small slice of the CDO he was managing. That way, the manager would have more incentive to manage the investment well, since he, too, was an investor. But small management firms rarely had money to invest. Some banks solved this problem by advancing money to managers such as Harding.

Chau's group managed two Citigroup CDOs -- 888 Tactical Fund and Jupiter High-Grade VII -- in which the bank loaned Harding money to buy risky pieces of the deal. The loans would be paid back out of the fees the managers took from the CDO and its investors. The loans were disclosed to investors in a few sentences among the hundreds of pages of legalese accompanying the deals.

In response to ProPublica's questions, Chau's lawyer said, "Harding Advisory's dealings with investment banks were proper and fully disclosed."

Citigroup made similar deals with other managers. The bank lent money to a manager called Vanderbilt Capital Advisors for its Armitage CDO, completed in March 2007.

Vanderbilt declined to comment. It couldn't be learned how much money Citigroup loaned or whether it was ever repaid.

Yet again banks had masked their true stakes in CDO. Banks were lending money to CDO managers so they could buy the banks' dodgy assets. If the managers couldn't pay the loans back -- and most were thinly capitalized -- the banks were on the hook for even more losses when the CDO business collapsed.

Goldman, Merrill and Others Get Tough

When the housing market deteriorated, banks took advantage of a little-used power they had over managers.

The way CDOs are put together, there is a brief period when the bonds picked by managers sit on the banks' balance sheets. Because the value of such assets can fall, banks reserved the right to overrule managers' selections.

According to numerous bankers, managers and investors, banks rarely wielded that veto until late 2006, after which it became common. Merrill was in the lead.

"I would go to Merrill and tell them that I wanted to buy, say, a Citi bond," recalls a CDO manager. "They would say 'no.' I would suggest a UBS bond, they would say 'no.' Eventually, you got the joke." Managers could choose assets to put into their CDOs but they had to come from Merrill CDOs. One rival investment banker says Merrill treated CDO managers the way Henry Ford treated his Model T customers: You can have any color you want, as long as it's black.

Once, Merrill's Ken Margolis pushed a manager to buy a CDO slice for a Merrill-produced CDO called Port Jackson that was completed in the beginning of 2007: "'You don't have to buy the deal but you are crazy if you don't because of your business,'" an executive at the management firm recalls Margolis telling him. "'We have a big pipeline and only so many more mandates to give you.' You got the message." In other words: Take our stuff and we'll send you more business. If not, forget it.

Margolis declined to comment on the incident.

"All the managers complained about it," recalls O'Driscoll, the former Credit Suisse banker who competed with other investment banks to put deals together and market them. But "they were indentured slaves." O'Driscoll recalls managers grumbling that Merrill in particular told them "what to buy and when to buy it."

Other big CDO-producing banks quickly adopted the practice.

A little-noticed document released this year during a congressional investigation into Goldman Sachs' CDO business reveals that bank's thinking. The firm wrote a November 2006 internal memorandum about a CDO called Timberwolf, managed by Greywolf, a small manager headed by ex-Goldman bankers. In a section headed "Reasons To Pursue," the authors touted that "Goldman is approving every asset" that will end up in the CDO. What the bank intended to do with that approval power is clear from the memo: "We expect that a significant portion of the portfolio by closing will come from Goldman's offerings."

When asked to comment whether Goldman's memo demonstrates that it had effective control over the asset selection process and that Greywolf was not in fact an independent manager, the bank responded: "Greywolf was an experienced, independent manager and made its own decisions about what reference assets to include. The securities included in Timberwolf were fully disclosed to the professional investors who invested in the transaction."

Greywolf declined to comment. One of the investors, Basis Capital of Australia, filed a civil lawsuit in federal court in Manhattan against Goldman over the deal. The bank maintains the lawsuit is without merit.

By March 2007, the housing market's signals were flashing red. Existing home sales plunged at the fastest rate in almost 20 years. Foreclosures were on the rise. And yet, to CDO buyer Peter Nowell's surprise, banks continued to churn out CDOs.

"We were pulling back. We couldn't find anything safe enough," says Nowell. "We were amazed that April through June they were still printing deals. We thought things were over."

Instead, the CDO machine was in overdrive. Wall Street produced $70 billion in mortgage CDOs in the first quarter of the year.

Many shareholder lawsuits battling their way through the court system today focus on this period of the CDO market. They allege that the banks were using the sales of CDOs to other CDOs to prop up prices and hide their losses.

"Citi's CDO operations during late 2006 and 2007 functioned largely to sell CDOs to yet newer CDOs created by Citi to house them," charges a pending shareholder lawsuit against the bank that was filed in federal court in Manhattan in February 2009. "Citigroup concocted a scheme whereby it repackaged many of these investments into other freshly-baked vehicles to avoid incurring a loss."

Citigroup described the allegations as "irrational," saying the bank's executives would never knowingly take actions that would lead to "catastrophic losses."

In the Hall of Mirrors, Myopic Rating Agencies

The portion of CDOs owned by other CDOs grew right alongside the market. What had been 5 percent of CDOs (remember the "bucket") now came to constitute as much as 30 or 40 percent of new CDOs. (Wall Street also rolled out CDOs that were almost entirely made up of CDOs, called CDO squareds.)

The ever-expanding bucket provided new opportunities for incestuous trades.

It worked like this: A CDO would buy a piece of another CDO, which then returned the favor. The transactions moved both CDOs closer to completion, when bankers and managers would receive their fees.

ProPublica's analysis shows that in the final two years of the business, CDOs with cross-ownership amounted to about one-fifth of the market, about $107 billion.

Here's an example from early May 2007:

A CDO called Jupiter VI bought a piece of a CDO called Tazlina II.

Tazlina II bought a piece of Jupiter VI.

Both Jupiter VI and Tazlina II were created by Merrill and were completed within a week of each other. Both were managed by small firms that did significant business with Merrill: Jupiter by Wing Chau's Harding, and Tazlina by Terwin Advisors. Chau did not respond to questions about this deal. Terwin Advisors could not reached.

Just a few weeks earlier, CDO managers completed a comparable swap between Jupiter VI and another Merrill CDO called Forge 1.

Forge has its own intriguing history. It was the only deal done by a tiny manager of the same name based in Tampa, Fla. The firm was started less than a year earlier by several former Wall Street executives with mortgage experience. It received seed money from Bryan Zwan, who in 2001 settled an SEC civil lawsuit over his company's accounting problems in a federal court in Florida. Zwan and Forge executives didn't respond to requests for comment.

After seemingly coming out of nowhere, Forge won the right to manage a $1.5 billion Merrill CDO. That earned Forge a visit from the rating agency Moody's.

"We just wanted to make sure that they actually existed," says a former Moody's executive. The rating agency saw that the group had an office near the airport and expertise to do the job.

Rating agencies regularly did such research on managers, but failed to ask more fundamental questions. The credit ratings agencies "did heavy, heavy due diligence on managers but they were looking for the wrong things: how you processed a ticket or how your surveillance systems worked," says an executive at a CDO manager. "They didn't check whether you were buying good bonds."

One Forge employee recalled in a recent interview that he was amazed Merrill had been able to find buyers so quickly. "They were able to sell all the tranches" -- slices of the CDO -- "in a fairly rapid period of time," said Rod Jensen, a former research analyst for Forge.

Forge achieved this feat because Merrill sold the slices to other CDOs, many linked to Merrill.

The ProPublica analysis shows that two Merrill CDOs, Maxim II and West Trade III, each bought pieces of Forge. Small managers oversaw both deals.

Forge, in turn, was filled with detritus from Merrill. Eighty-two percent of the CDO bonds owned by Forge came from other Merrill deals.

Citigroup did its own version of the shuffle, as these three CDOs demonstrate:

A CDO called Octonion bought some of Adams Square Funding II.

Adams Square II bought a piece of Octonion.

A third CDO, Class V Funding III, also bought some of Octonion.

Octonion, in turn, bought a piece of Class V Funding III.

All of these Citi deals were completed within days of each other. Wing Chau was once again a central player. His firm managed Octonion. The other two were managed by a unit of Credit Suisse. Credit Suisse declined to comment.

Not all cross-ownership deals were consummated.

In spring 2007, Deutsche Bank was creating a CDO and found a manager that wanted to take a piece of it. The manager was overseeing a CDO that Merrill was assembling. Merrill blocked the manager from putting the Deutsche bonds into the Merrill CDO. A former Deutsche Bank banker says that when Deutsche Bank complained to Andy Phelps, a Merrill CDO executive, Phelps offered a quid pro quo: If Deutsche was willing to have the manager of its CDO buy some Merrill bonds, Merrill would stop blocking the purchase. Phelps declined to comment.

The Deutsche banker, who says its managers were independent, recalls being shocked: "We said we don't control what people buy in their deals." The swap didn't happen.

The Missing Regulators and the Aftermath

In September 2007, as the market finally started to catch up with Merrill Lynch, Ken Margolis left the firm to join Wing Chau at Harding.

Chau and Margolis circulated a marketing plan for a new hedge fund to prospective investors touting their expertise in how CDOs were made and what was in them. The fund proposed to buy failed CDOs -- at bargain basement prices. In the end, Margolis and Chau couldn't make the business work and dropped the idea.

Why didn't regulators intervene during the boom to stop the self-dealing that had permeated the CDO market?

No one agency had authority over the whole business. Since the business came and went in just a few years, it may have been too much to expect even assertive regulators to comprehend what was happening in time to stop it.

While the financial regulatory bill passed by Congress in July creates more oversight powers, it's unclear whether regulators have sufficient tools to prevent a replay of the debacle.

In just two years, the CDO market had cut a swath of destruction. Partly because CDOs had bought so many pieces of each other, they collapsed in unison. Merrill Lynch and Citigroup, the biggest perpetrators of the self-dealing, were among the biggest losers. Merrill lost about $26 billion on mortgage CDOs and Citigroup about $34 billion.

Additional reporting by Kitty Bennett, Krista Kjellman Schmidt, Lisa Schwartz and Karen Weise.

Correction: This story previously reported that there were 85 instances during 2006 and 2007 in which two complex securities known as collateralized debt obligations bought pieces of each others' "unsold" inventory. In fact, there were some instances when this cross-exposure occurred through later transactions. The banks sometimes used such transactions to minimize their own exposure to CDOs they had created.

An interactive graphic we published includes at least one example of cross-exposure that did not involve "unsold" inventory. A CDO called Tourmaline III made a sidebet in 2007 that mirrored the performance of a piece of a CDO called Zais Investment Grade 8; that same year Zais 8 bought a piece of Tourmaline III. Both CDOs were underwritten by Deutsche Bank.

© 2010 ProPublica, Inc.

By Jake Bernstein and Jesse Eisinger

Two years before the financial crisis hit, Merrill Lynch confronted a serious problem. No one, not even the bank's own traders, wanted to buy the supposedly safe portions of the mortgage-backed securities Merrill was creating.

Bank executives came up with a fix that had short-term benefits and long-term consequences. They formed a new group within Merrill, which took on the bank's money-losing securities. But how to get the group to accept deals that were otherwise unprofitable? They paid them. The division creating the securities passed portions of their bonuses to the new group, according to two former Merrill executives with detailed knowledge of the arrangement.

The executives said this group, which earned millions in bonuses, played a crucial role in keeping the money machine moving long after it should have ground to a halt.

"It was uneconomic for the traders" -- that is, buyers at Merrill -- "to take these things," says one former Merrill executive with knowledge of how it worked.

Within Merrill Lynch, some traders called it a "million for a billion" -- meaning a million dollars in bonus money for every billion taken on in Merrill mortgage securities. Others referred to it as "the subsidy." One former executive called it bribery. The group was being compensated for how much it took, not whether it made money.

The group, created in 2006, accepted tens of billions of dollars of Merrill's Triple A-rated mortgage-backed assets, with disastrous results. The value of the securities fell to pennies on the dollar and helped to sink the iconic firm. Merrill was sold to Bank of America, which was in turn bailed out by taxpayers.

What became of the bankers who created this arrangement and the traders who took the now-toxic assets? They walked away with millions. Some still hold senior positions at prominent financial firms.

Washington is now grappling with new rules about how to limit Wall Street bonuses in order to better align bankers' behavior with the long-term health of their bank. Merrill's arrangement, known only to a small number of executives at the firm, shows just how damaging the misaligned incentives could be.

ProPublica has published a series of articles throughout the year about how Wall Street kept the money machine spinning. Our examination has shown that as banks faced diminishing demand for every part of the complex securities known as collateralized debt obligations, or CDOs, Merrill and other firms found ways to circumvent the market's clear signals.

The mortgage securities business was supposed to have a firewall against this sort of conflict of interest.

Banks like Merrill bought pools of mortgages and bundled them into securities, eventually making them into CDOs. Merrill paid upfront for the mortgages, but this outlay was quickly repaid as the bank made the securities and sold them to investors. The bankers doing these deals had a saying: We're in the moving business, not the storage business.

Executives producing the securities were not allowed to buy much of their own product; their pay was calculated by the revenues they generated. For this reason, decisions to hold a Merrill-created security for the long term were made by independent traders who determined, in essence, that the Merrill product was as good or better than what was available in the market.

By creating more CDOs, banks prolonged the boom. Ultimately the global banking system was saddled with hundreds of billions of dollars worth of toxic assets, triggering the 2008 implosion and throwing millions of people out of work and sending the global economy into a tailspin from which it has not yet recovered.

Executives who oversaw Merrill's CDO buying group dispute aspects of this account. One executive involved acknowledges that fees were shared, but says it was not a "formalized arrangement" and was instead done on a "case-by-case basis." Calling the arrangement bribery "is ridiculous," he says.

The executives also say the new group didn't drive Merrill's CDO production. In fact, they say the group was part of a plan to reduce risk by consolidating the unwanted assets into one place. The traders simply provided a place to put them. "We were managing and booking risk that was already in the firm and couldn't be sold," says one person who worked in the group.

A month before the group was created, Merrill Lynch owned $7.2 billion of the seemingly safe investments, according to an internal risk management report. By the time the CDO losses started mounting in July 2007, that figure had skyrocketed to $32.2 billion, most of which was held by the new group.

The origins of Merrill's crisis came at the beginning of 2006, when the bank's biggest customer for the supposedly safe assets -- the giant insurer AIG -- decided to stop buying the assets, known as "super-senior," after becoming worried that perhaps they weren't so safe after all.

The super-senior was the top portion of CDOs, meaning investors who owned it were the first to be compensated as homeowners paid their mortgages, and last in line to take losses should people become delinquent. By the fall of 2006, the housing market was dipping, and big insurance companies, pension funds and other institutional investors were turning away from any investments tied to mortgages.

Until that point, Merrill's own traders had been making money on purchases of super-senior debt. The traders were careful about their purchases. They would buy at prices they regarded as attractive and then make side bets -- what are known as hedges -- that would pay off if the value of the securities fell. This approach allowed the traders to make money for Merrill while minimizing the bank's risk.

It also was personally profitable. Annual bonuses for traders -- which can make up more than 75 percent of total compensation -- are largely based on how much money each individual makes for the firm.

By the middle of 2006, the Merrill traders who bought mortgage securities were often clashing with the powerful division, run by Harin De Silva and Ken Margolis, which created and sold the CDOs. At least three traders began to refuse to buy CDO pieces created by De Silva and Margolis' division, according to several former Merrill employees. (De Silva and Margolis didn't respond to requests for comment.)

In late September, Merrill created a $1.5 billion CDO called Octans, named after a constellation in the southern sky. It had been built at the behest of a hedge fund, Magnetar, and filled will some of the riskier mortgage-backed securities and CDOs. (As we reported in April with Chicago Public Radio's This American Life and NPR's Planet Money, Magnetar had helped create more than $40 billion worth of CDOs with a variety of banks, and bet against many of those CDOs as part of a strategy to profit from the decline in the housing market.)

In an incident reported by the Wall Street Journal ($) in April 2008, a Merrill trader looked over the contents of Octans and refused to buy the super-senior, believing that he should not be buying what no one else wanted. The trader was sidelined and eventually fired. (The same Journal article also reported that the new group had taken the majority of Merrill's super-seniors.)

The difficulty in finding buyers should have been a warning signal: If the market won't buy a product, maybe the bank should stop making it.

Instead, a Merrill executive, Dale Lattanzio, called a meeting, attended by among others the heads of the CDO sales group -- Margolis and De Silva -- and a trader, Ranodeb Roy. According to a person who attended the meeting, they discussed creating a special group under Roy to accept super-senior slices. (Lattanzio didn't respond to requests for comment.)